Sorry for the late reply, you have brought up a few interesting points.

1) As a primary home, would it be safe to say that we don’t really need to consider the investment nature of the property.

For me, no. If you can live in the same apartment regardless of renting/buying, what matters is, how much you have to pay for it. Let's ignore being kicked out by landlord that kind of uncontrollable things. Even if you buy an apartment, there are many things uncontrollable, including compulsory contribution to the building maintenance, someone died near your unit and pulls down your property price as being closed to a 凶宅.

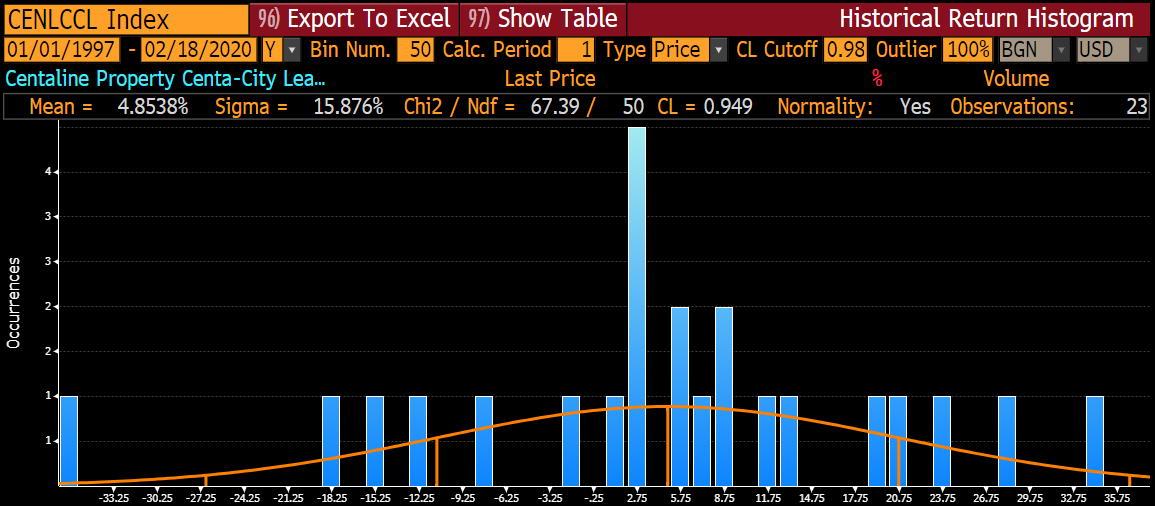

So what really matters, if whether you put your money into the right place. TOO MANY people only focus on my assumption of making 10% profit annually. But to be very honest, that is not the emphasis of my words. I took the past 2x years HK property pricing data ( cos the pricing index started in 1997) and drew a normal distribution (significant 95%).

What we see is, the annual growth rate of the so called booming HK property price, is only 4.85%. Given the inflation of the past 30 years is around 2.6%. So you see, the actual gain from the property appreciation is only 2.25%, which is the current mortgage rate.

For those who understands what I said, you see that the appreciation of the property can only offset the current p-3=2.25% mortgage lending rate...Then, my question back to you is, is it really worth locking your opportunity cost here?

Of course, throughout the years, you can draw extra cash from the property by doing mortgage refinancing. But me as a non-property owner, i can also utilize personal loan.

完全駁唔到我d points

完全駁唔到我d points

p loan tenor幾長?有冇30年?

p loan tenor幾長?有冇30年? 唔好話咩情況需要有變第日可能買呀,你個annual return 10% 計劃一定正過買樓,作為rational investor身家十億都唔應該買樓,買左就做我契弟架喇,cfa

唔好話咩情況需要有變第日可能買呀,你個annual return 10% 計劃一定正過買樓,作為rational investor身家十億都唔應該買樓,買左就做我契弟架喇,cfa