唔熟quan fin

Basic Signal processing 都好多transform

再玩上去好多FFT, 好多real analysis 野

Introduction to Stochastic Calculus & Application in Finance

宇智波月巴

674 回覆

359 Like

8 Dislike

第 1 頁第 2 頁第 3 頁第 4 頁第 5 頁第 6 頁第 7 頁第 8 頁第 9 頁第 10 頁第 11 頁第 12 頁第 13 頁第 14 頁第 15 頁第 16 頁第 17 頁第 18 頁第 19 頁第 20 頁第 21 頁第 22 頁第 23 頁第 24 頁第 25 頁第 26 頁第 27 頁

ee仔lm

其實quant fin都會用嗰堆transform

如果講完change of measure仲未嚇走曬啲人嘅話我可能會講少少

如果講完change of measure仲未嚇走曬啲人嘅話我可能會講少少

lm

fft in option pricing

2008 之前好暢旺, derivatives 五花八門,日新月異, ibanks 係咁請人做 monte carlo, finite difference, 總知任何方法做 pricing。

但係爆左煲後,監管又嚴左,而家冇呢支歌唱。佢話而家最 hit 一係做 portfolio, 一係做 execution.

但係爆左煲後,監管又嚴左,而家冇呢支歌唱。佢話而家最 hit 一係做 portfolio, 一係做 execution.

考埋midterm慢慢睇

最怕 complex analysis

睇睇下有d想返番去讀書既年代

利申:吾城QFRM grad,成績差乞食中

利申:吾城QFRM grad,成績差乞食中

應該關係不大 stochastic calculus 係 w.r.t. time, 即係要用 time series data, 而 big data 通常係 cross sectional.

Ching 可以跟住呢個flow 開個YouTube channel 用廣東話教應該好快好多view

推

Review for Part 1 and 2 (up to Ito's lemma)

小弟最痛苦嗰科midterm終於完咗 又可以繼續出post

又可以繼續出post

之前都講過今次會整一個review先 幫大家整理一下我地依家知道嘅野

順便補充多少少關於financial derivative同stat嘅知識

Financial derivative

--------------------------------------------------

Basic concept of Stat

--------------------------------------------------

Wiener process

--------------------------------------------------

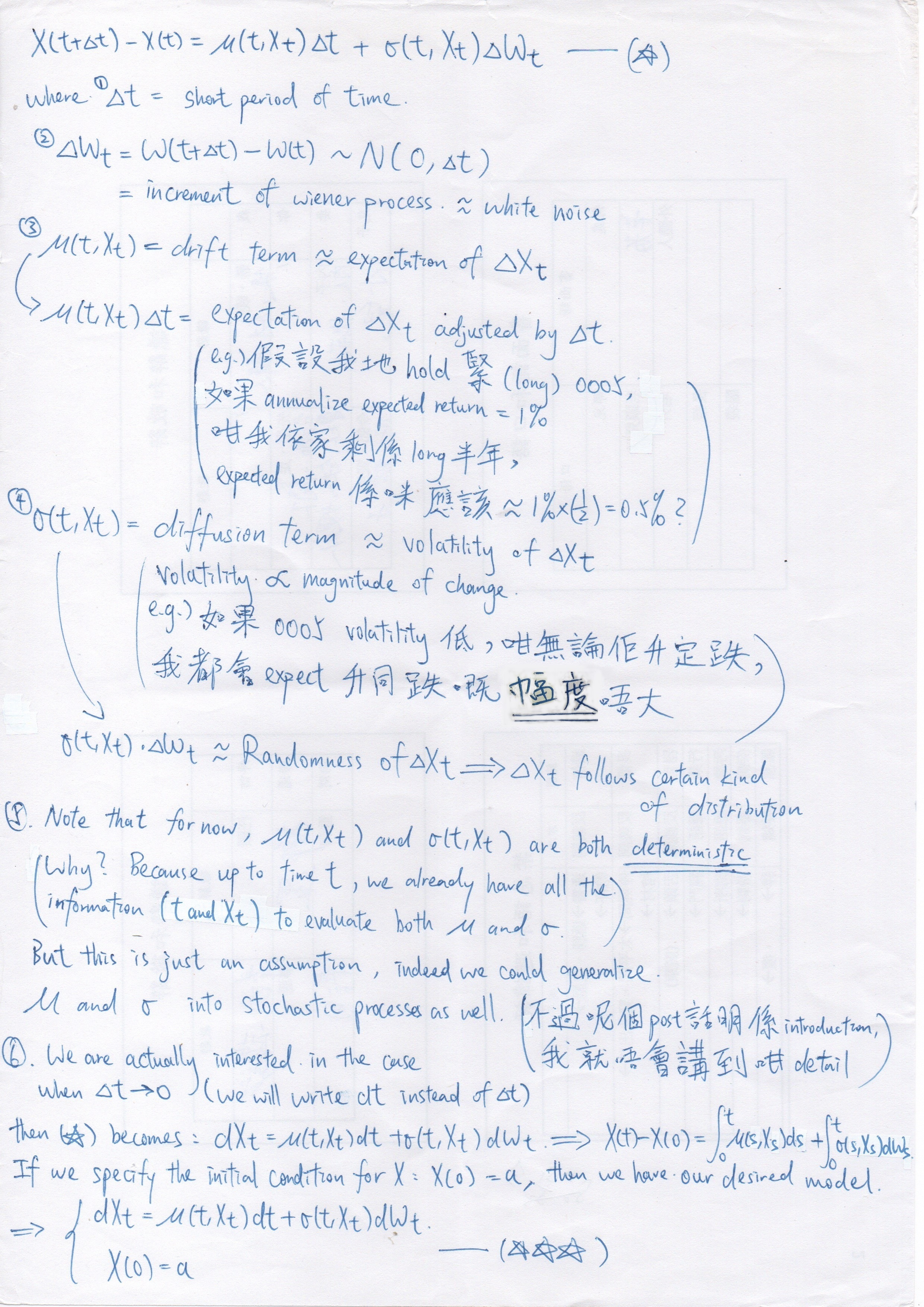

Model setting

--------------------------------------------------

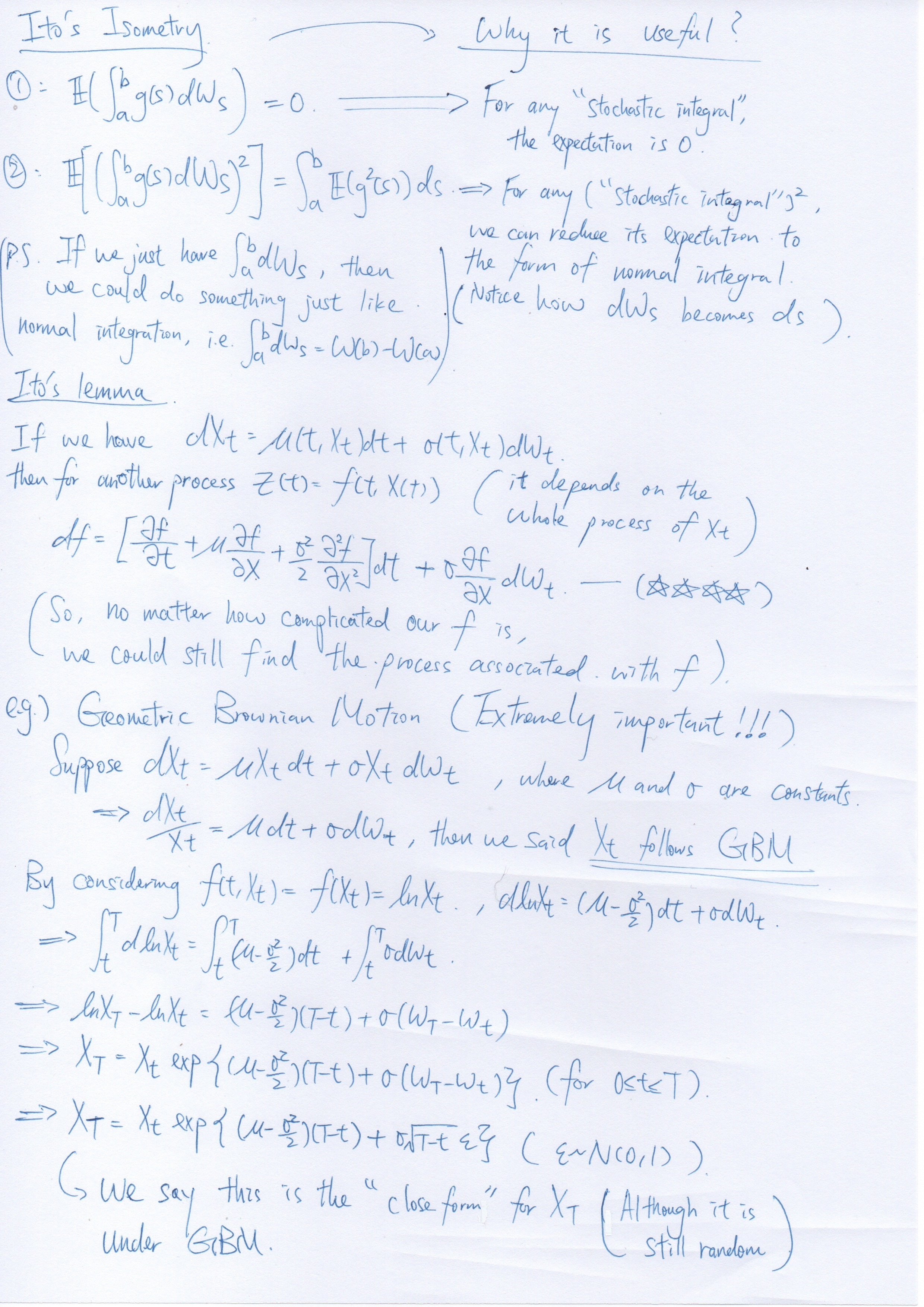

Ito's isometry and lemma

--------------------------------------------------

今日晏啲就會出black scholes嘅第一part --- Black scholes equation

請大家耐心再等多陣

小弟最痛苦嗰科midterm終於完咗

又可以繼續出post之前都講過今次會整一個review先 幫大家整理一下我地依家知道嘅野

順便補充多少少關於financial derivative同stat嘅知識

Financial derivative

--------------------------------------------------

Basic concept of Stat

--------------------------------------------------

Wiener process

--------------------------------------------------

Model setting

--------------------------------------------------

Ito's isometry and lemma

--------------------------------------------------

今日晏啲就會出black scholes嘅第一part --- Black scholes equation

請大家耐心再等多陣

我用廣東話教肯定教到口疾疾

況且英文底唔差嘅話 去返啲英文channel (khan academy之類) 學上面呢堆野會易明好多

況且英文底唔差嘅話 去返啲英文channel (khan academy之類) 學上面呢堆野會易明好多

可唔可以講下risk neutral 係d咩黎

SDE直頭係讀mathematics of finance/ derivative pricing時候嘅惡夢

正呀,大學讀financial engineering,啲數唔記得晒,當溫習返

risk neutral我陣間就會開始講少少

不過其實要到feynman kac formula先會講到一個完整嘅full picture比大家聽

不過其實要到feynman kac formula先會講到一個完整嘅full picture比大家聽

pricing method

3.) Black Scholes Merton Model

唔知大家有冇聽過Black, Scholes同Merton 呢三個人名呢

呢三個人可以話係Modern finance發展得咁快嘅功臣之一

基本上任何一個financial market背後都可以見到佢地嘅蹤影

相信有唔少人都買過call/put (認購證/認沽證) 呢類option

大家有冇好奇過究竟呢啲derivative嘅價錢係點計出黎?

仲有 眼利嘅朋友喺買呢啲option嘅時候可能會留意到

有一樣好奇怪嘅嘢叫"Implied volatility"

Volatility大家都明 但係加個implied係頭又係點解

大家唔洗心急 一切嘅問題都會係下面慢慢迎刃而解

而BSM model強大之處就在於佢可以幫大家搵到一個derivative嘅價錢嘅"close form"出黎

(記唔記得我講過SDE其實好難有close form? )

)

當然佢用途唔止咁 慢慢大家就會知道點解呢個model咁重要

(background) No arbitrage pricing

喺講任何嘢之前 我地仲有一個非常非常重要嘅concept要講清楚

呢個就係no arbitrage pricing啦

Arbitrage (套利) 通常就係指risk-less profit

呢到"risk-less"嘅意思就係照字面解 要完全零風險

無論個market點樣郁 郁幾多都好

你都可以依照一套方法 係任何情況下都有profit 而呢一舊profit係必然會賺到返黎

咁嘅話我地就會話個market有arbitrage opportunity

( 大家口中所講嘅risk-free rate係現實其實未必等同於risk-less

大家口中所講嘅risk-free rate係現實其實未必等同於risk-less

因為擺deposit係銀行收risk-free rate根本就唔係risk-less 2008年已經有好例子比大家睇 )

)

而通常我地都會consider一個比較簡單嘅case先

假設依家個market得一隻stock 一隻derivative 一個risk-free rate

咁點check有冇arbitrage opportunity? 我地就要靠上面三樣嘢去砌一個portfolio出黎

(e.g. short sell 1 share of stock, long 1 share of call, deposit the money I get from short selling the stock in bank to receive risk-free rate )

然後我地就要睇下會唔會有一個portfolio係符合下面是但一個case

如果比你搵個一個咁嘅portfolio 咁你就可以話呢個market有arbitrage

咁大家可能又會問: 點解個market無端端會有arbitrage?

我地首先去返比較簡單嘅case先 (1 stock, 1 derivative, 1 risk-free rate)

interest rate其實係depends on money demand同money supply

stock price就係depends on本身間公司嘅underlying value

我地再假設stock price係一個fair estimate of a company's underlying value 同埋 interest rate已經比money demand同supply determine咗出黎

咁令到呢個market有arbitrage嘅元凶只有一個 --- 就係嗰隻derivative

因為derivative嘅價錢set錯咗(not its fair price)

所以就令到呢個simple market有risk-less profit

咁當然個market都唔係白痴 所有人都會意識到呢一點

而當derivative嘅價錢本身定得太低 咁就會愈黎愈多人買 價錢慢慢就會被推高

而如果定得太高 咁就會愈黎愈多人賣 價錢慢慢被推低

總之根據demand&supply 慢慢derivative嘅價錢就會去返fair price

冇人再可以有任何方法賺到risk-less profit => Arbitrage opportunity does not exist

之但係price derivative嘅人都唔係白痴

佢地當然知咩係arbitrage 亦都知就算一開頭有arbitrage都好 最終靠個market都可以achieve到fair price

個問題就係佢唔會咁傻仔比我地賺一開頭嗰啲risk-less profit呀嘛

而呢個就係所謂嘅no arbitrage pricing --- 一開頭就將derivative嘅價錢set做fair price

(其實唔單止一開頭 任何time point都唔應該有arbitrage)

咁就唔會有任何arbitrage出現

------------------------------------------------------------------------

(a) Black Scholes Equation

講咗咁耐arbitrage 我地終於要入戲肉

首先講下Black Scholes Model嘅setting同assumption先

大家都知道任何model都冇可能同現實100%一樣 (就算強如particle physics嘅standard model都唔係)

所以適量嘅assumption係必須嘅 同時亦都可以令我地之後輕鬆啲

基本assumptions如下:

--------------------------------------------------------------

下個cm繼續 我又唔夠位寫

唔知大家有冇聽過Black, Scholes同Merton 呢三個人名呢

呢三個人可以話係Modern finance發展得咁快嘅功臣之一

基本上任何一個financial market背後都可以見到佢地嘅蹤影

相信有唔少人都買過call/put (認購證/認沽證) 呢類option

大家有冇好奇過究竟呢啲derivative嘅價錢係點計出黎?

仲有 眼利嘅朋友喺買呢啲option嘅時候可能會留意到

有一樣好奇怪嘅嘢叫"Implied volatility"

Volatility大家都明 但係加個implied係頭又係點解

大家唔洗心急 一切嘅問題都會係下面慢慢迎刃而解

而BSM model強大之處就在於佢可以幫大家搵到一個derivative嘅價錢嘅"close form"出黎

(記唔記得我講過SDE其實好難有close form?

)當然佢用途唔止咁 慢慢大家就會知道點解呢個model咁重要

(background) No arbitrage pricing

喺講任何嘢之前 我地仲有一個非常非常重要嘅concept要講清楚

呢個就係no arbitrage pricing啦

Arbitrage (套利) 通常就係指risk-less profit

呢到"risk-less"嘅意思就係照字面解 要完全零風險

無論個market點樣郁 郁幾多都好

你都可以依照一套方法 係任何情況下都有profit 而呢一舊profit係必然會賺到返黎

咁嘅話我地就會話個market有arbitrage opportunity

(

大家口中所講嘅risk-free rate係現實其實未必等同於risk-less因為擺deposit係銀行收risk-free rate根本就唔係risk-less 2008年已經有好例子比大家睇

)而通常我地都會consider一個比較簡單嘅case先

假設依家個market得一隻stock 一隻derivative 一個risk-free rate

咁點check有冇arbitrage opportunity? 我地就要靠上面三樣嘢去砌一個portfolio出黎

(e.g. short sell 1 share of stock, long 1 share of call, deposit the money I get from short selling the stock in bank to receive risk-free rate )

然後我地就要睇下會唔會有一個portfolio係符合下面是但一個case

Case I:

一開頭(t=0) payoff必然>0 然後到maturity (t=T) payoff必然>= 0

Case II:

一開頭(t=0) payoff必然=0 然後到maturity (t=T) payoff必然>0

如果比你搵個一個咁嘅portfolio 咁你就可以話呢個market有arbitrage

咁大家可能又會問: 點解個market無端端會有arbitrage?

我地首先去返比較簡單嘅case先 (1 stock, 1 derivative, 1 risk-free rate)

interest rate其實係depends on money demand同money supply

stock price就係depends on本身間公司嘅underlying value

我地再假設stock price係一個fair estimate of a company's underlying value 同埋 interest rate已經比money demand同supply determine咗出黎

咁令到呢個market有arbitrage嘅元凶只有一個 --- 就係嗰隻derivative

因為derivative嘅價錢set錯咗(not its fair price)

所以就令到呢個simple market有risk-less profit

咁當然個market都唔係白痴 所有人都會意識到呢一點

而當derivative嘅價錢本身定得太低 咁就會愈黎愈多人買 價錢慢慢就會被推高

而如果定得太高 咁就會愈黎愈多人賣 價錢慢慢被推低

總之根據demand&supply 慢慢derivative嘅價錢就會去返fair price

冇人再可以有任何方法賺到risk-less profit => Arbitrage opportunity does not exist

之但係price derivative嘅人都唔係白痴

佢地當然知咩係arbitrage 亦都知就算一開頭有arbitrage都好 最終靠個market都可以achieve到fair price

個問題就係佢唔會咁傻仔比我地賺一開頭嗰啲risk-less profit呀嘛

而呢個就係所謂嘅no arbitrage pricing --- 一開頭就將derivative嘅價錢set做fair price

(其實唔單止一開頭 任何time point都唔應該有arbitrage)

咁就唔會有任何arbitrage出現

------------------------------------------------------------------------

(a) Black Scholes Equation

講咗咁耐arbitrage 我地終於要入戲肉

首先講下Black Scholes Model嘅setting同assumption先

大家都知道任何model都冇可能同現實100%一樣 (就算強如particle physics嘅standard model都唔係)

所以適量嘅assumption係必須嘅 同時亦都可以令我地之後輕鬆啲

基本assumptions如下:

1.) Market consists of at least one stock and one risk-less asset (i.e. money market, cash, or bond)

2.) The rate of return on the risk-less asset is constant and thus called the risk-free interest rate

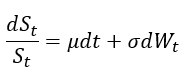

3.) Stock price follows Geometric Brownian motion with constant μ and σ

4.) The stock does not pay a dividend (We can generalize it later)

5.) There is no arbitrage opportunity in the market

6.) It is possible to borrow and lend any amount, even fractional, of cash at the risk-less rate

7.) It is possible to buy and sell any amount, even fractional, of the stock (this includes short selling)

8.) No transaction cost (i.e. friction-less market) (We can generalize it later)

--------------------------------------------------------------

下個cm繼續

我又唔夠位寫3.) Black Scholes Merton Model

(a) Black Scholes Equation (cont.)

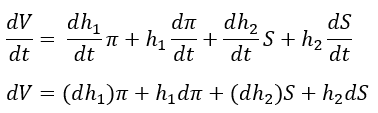

然後我地就假設有一隻derivative (based on stock) 係呢個market

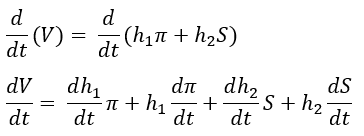

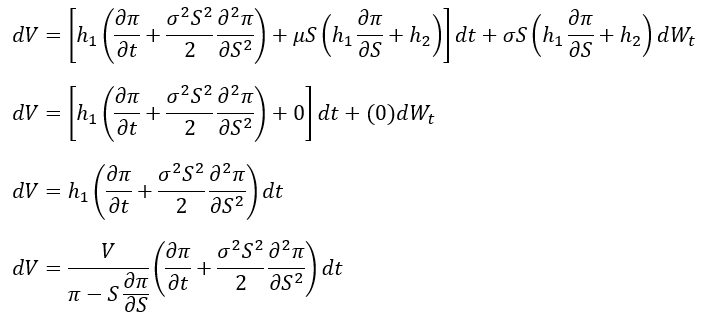

咁我地就可以consider以下呢一個portfolio:

而h1同h2就係分別對應住derivative同stock嘅weight (記住我地assume咗可以buy/sell fractional amount)

(p.s. π當然係function of t and S_t , 而S_t當然係function of t)

跟住我地就考慮下呢個portfolio嘅change in value w.r.t time (apply d/dt)

再之後應該點? 咪又係abuse notation

見唔見到所有term下面都係除dt? 我地一嘢約曬佢

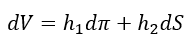

跟住我地就要介紹另一個新嘅concept --- self-finance portfolio

個原理好簡單 就用返我地依家呢個portfolio V做例子

For e.g. 我賣左(short) 2 unit of stock 咁我得返黎嘅錢就要全部invest落derivative

同理 如果我買左(long) 2 unit of stock 咁即係我之前就已經賣左啲derivative 所以先會有錢買stock

簡單講就係唔會有額外嘅錢流出呢一個portfolio 亦都唔會有額外嘅錢流入

咁我地就可以諗下 呢個portfolio V 嘅change (dV) 其實真正depends on 啲咩?

如果V係self-financing 咁佢嘅change (dV) 就唔應該depends on change of weights (dh_1, dh_2)

所以我地可以將dV reduces做下面呢個樣:

係咪即刻順眼好多呢

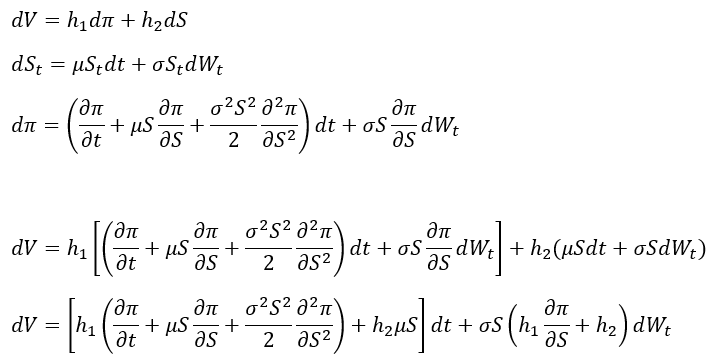

聰明嘅朋友睇到呢步其實都大概估到跟住我想做咩

大家仲記唔記得dS係咩? (Hint: Stock price follows GBM)

大家又記唔記得可以點搵dπ? (Hint: Ito's lemma)

我地既然知道曬所有嘢 咁就梗係plug曬落條式裏面啦

Now what

我地又要再consider一樣嘢

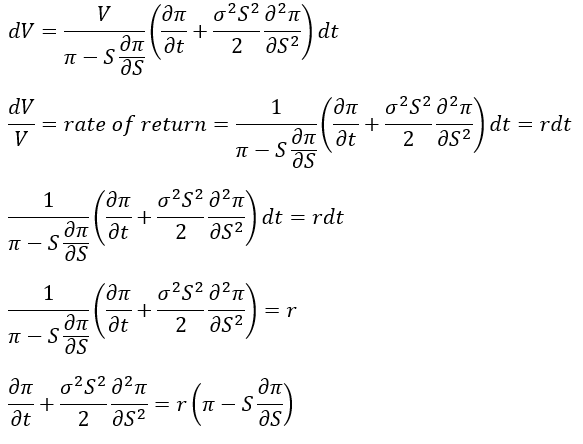

如果呢個portfolio係risk-less嘅(in short period of time dt) 咁會發生咩事?

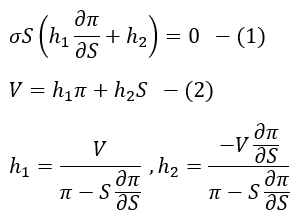

首先 dW_t前面嘅coefficient應該要 = 0

點解? 因為一個riskless portfolio係唔會有任何randomness

而第二點就係你嘅rate of return of portfolio V一定係risk-free rate

所以我地可以consider下面呢set simultaneous equations:

咁即係話 當我地分別set h_1同h_2 做呢兩舊嘢

成個portfolio V就係in short period of time (dt) risk-less

而當我地代返呢一set h_1,h_2入去dV

dW_t嘅coefficient就會變0

同時留意其實dt嘅coefficient入面都有一個舊嘢係同dW_t嘅coefficient一模一樣

所以都係會變埋0

根據埋上面第二點 rate of return一定係risk-free rate

所以我地有以下嘅結論:

而當你整理好條pde 你就會發現

原來我地已經寫低咗 Black Scholes equation

(當然我地都要assume埋個derivative at maturity嘅payoff係等於一個function of S)

--------------------------------------------------------------------

(Things to take away)

首先我想大家思考一下我地啱先究竟做過啲乜

我地明明係plug in咗兩條SDE入去dV裏面

但係最尾我地竟然chok到條pde出黎?

而呢條pde仲要係直接話到比我地聽derivative嘅price應該係點樣

呢個example其實就show到比我地睇 實制上SDE同PDE就係互相connected

所以如果你solve pde好勁嘅話 其實係可以直接靠pde裏面嘅方法去solve一個solution出黎

不過小弟自問功力就真係唔夠深做唔到

其次 大家記唔記得原本個stock係follows GBM?

咁即係話expected rate of return of stock = μ

而呢個μ其實可以用time series data approximate出黎

但係你有冇發覺 係Black scholes equation入面個μ唔見咗?

成件事係咪好神奇?

呢個其實就係所謂嘅risk-neutral pricing 一個非常神奇嘅concept

本身underlying嘅mean or drift or 乜都好 其實對derivative黎講根本就唔重要

我地只需要知道risk-free rate就可以做pricing

或者換個角度講 只有用risk-free rate去price derivative 我地先會計到佢嘅fair price

詳細嘅detail我係下一part就會慢慢講解

-----------------------------------------------------------------

依家我地得條pde 冇理由就咁收手㗎係咪?

我下面仲有咁多個section 好明顯就係會由black scholes equation搵到solution出黎

而下一個section: Feynman-Kac formula 就係幫我地搵solution嘅一個Theorem

同時大家亦都會對何謂Risk-neutral pricing有更深刻嘅理解

大家又要等我幾日

(a) Black Scholes Equation (cont.)

然後我地就假設有一隻derivative (based on stock) 係呢個market

咁我地就可以consider以下呢一個portfolio:

而h1同h2就係分別對應住derivative同stock嘅weight (記住我地assume咗可以buy/sell fractional amount)

(p.s. π當然係function of t and S_t , 而S_t當然係function of t)

跟住我地就考慮下呢個portfolio嘅change in value w.r.t time (apply d/dt)

再之後應該點? 咪又係abuse notation

見唔見到所有term下面都係除dt? 我地一嘢約曬佢

跟住我地就要介紹另一個新嘅concept --- self-finance portfolio

個原理好簡單 就用返我地依家呢個portfolio V做例子

For e.g. 我賣左(short) 2 unit of stock 咁我得返黎嘅錢就要全部invest落derivative

同理 如果我買左(long) 2 unit of stock 咁即係我之前就已經賣左啲derivative 所以先會有錢買stock

簡單講就係唔會有額外嘅錢流出呢一個portfolio 亦都唔會有額外嘅錢流入

咁我地就可以諗下 呢個portfolio V 嘅change (dV) 其實真正depends on 啲咩?

如果V係self-financing 咁佢嘅change (dV) 就唔應該depends on change of weights (dh_1, dh_2)

所以我地可以將dV reduces做下面呢個樣:

係咪即刻順眼好多呢

聰明嘅朋友睇到呢步其實都大概估到跟住我想做咩

大家仲記唔記得dS係咩? (Hint: Stock price follows GBM)

大家又記唔記得可以點搵dπ? (Hint: Ito's lemma)

我地既然知道曬所有嘢 咁就梗係plug曬落條式裏面啦

Now what

我地又要再consider一樣嘢

如果呢個portfolio係risk-less嘅(in short period of time dt) 咁會發生咩事?

首先 dW_t前面嘅coefficient應該要 = 0

點解? 因為一個riskless portfolio係唔會有任何randomness

而第二點就係你嘅rate of return of portfolio V一定係risk-free rate

所以我地可以consider下面呢set simultaneous equations:

咁即係話 當我地分別set h_1同h_2 做呢兩舊嘢

成個portfolio V就係in short period of time (dt) risk-less

而當我地代返呢一set h_1,h_2入去dV

dW_t嘅coefficient就會變0

同時留意其實dt嘅coefficient入面都有一個舊嘢係同dW_t嘅coefficient一模一樣

所以都係會變埋0

根據埋上面第二點 rate of return一定係risk-free rate

所以我地有以下嘅結論:

而當你整理好條pde 你就會發現

原來我地已經寫低咗 Black Scholes equation

(當然我地都要assume埋個derivative at maturity嘅payoff係等於一個function of S)

--------------------------------------------------------------------

(Things to take away)

首先我想大家思考一下我地啱先究竟做過啲乜

我地明明係plug in咗兩條SDE入去dV裏面

但係最尾我地竟然chok到條pde出黎?

而呢條pde仲要係直接話到比我地聽derivative嘅price應該係點樣

呢個example其實就show到比我地睇 實制上SDE同PDE就係互相connected

所以如果你solve pde好勁嘅話 其實係可以直接靠pde裏面嘅方法去solve一個solution出黎

不過小弟自問功力就真係唔夠深做唔到

其次 大家記唔記得原本個stock係follows GBM?

咁即係話expected rate of return of stock = μ

而呢個μ其實可以用time series data approximate出黎

但係你有冇發覺 係Black scholes equation入面個μ唔見咗?

成件事係咪好神奇?

呢個其實就係所謂嘅risk-neutral pricing

一個非常神奇嘅concept本身underlying嘅mean or drift or 乜都好 其實對derivative黎講根本就唔重要

我地只需要知道risk-free rate就可以做pricing

或者換個角度講 只有用risk-free rate去price derivative 我地先會計到佢嘅fair price

詳細嘅detail我係下一part就會慢慢講解

-----------------------------------------------------------------

依家我地得條pde 冇理由就咁收手㗎係咪?

我下面仲有咁多個section 好明顯就係會由black scholes equation搵到solution出黎

而下一個section: Feynman-Kac formula 就係幫我地搵solution嘅一個Theorem

同時大家亦都會對何謂Risk-neutral pricing有更深刻嘅理解

大家又要等我幾日