Introduction to Stochastic Calculus & Application in Finance

宇智波月巴

674 回覆

359 Like

8 Dislike

Yeah anything is better than nothing and they were looking for a PhD intern so I just applied. Also I’m in Melbourne so Sydney is close.

It will be a lot easier to find a full time role with an internship. Anyways They still haven’t sent me the official offer yet so just keep it under wraps and fingers crossed.

It will be a lot easier to find a full time role with an internship. Anyways They still haven’t sent me the official offer yet so just keep it under wraps and fingers crossed.

Derivative Pricing

Risk Management

投行出隻新product如果唔識呢堆嘢佢地點price?

如果公司自己internal唔識MTM佢地點做risk management?

啲greek全部唔知點計 CVA又唔識計 咁好快2008發生過嘅嘢又會嚟多次

有時唔係predict到個股市先叫有用

何況你話你predict到我都唔會信你

random process你點predict? 我就算比個95%CI你都係冇意思 個CI會大到同冇講過嘢冇分別

Risk Management

投行出隻新product如果唔識呢堆嘢佢地點price?

如果公司自己internal唔識MTM佢地點做risk management?

啲greek全部唔知點計 CVA又唔識計 咁好快2008發生過嘅嘢又會嚟多次

有時唔係predict到個股市先叫有用

何況你話你predict到我都唔會信你

random process你點predict? 我就算比個95%CI你都係冇意思 個CI會大到同冇講過嘢冇分別

BS只係最簡單嗰個model

亦都係一個充滿問題嘅model

Stochastic volatility點算?

Stochastic interest rate又點算?

點樣quantify/model credit risk?

亦都係一個充滿問題嘅model

Stochastic volatility點算?

Stochastic interest rate又點算?

點樣quantify/model credit risk?

呢堆嘢全部都有用

如果你剩係用我呢個post暫時講過嘅嘢去judge stoc cal有冇用

咁我只可以講你真係太天真

同埋我一開頭都講呢個post係introduction

我唔會亦都冇可能講到去LIBOR market model嗰啲位

我依家講嘅嘢只係basic 如果你再另外睇書讀深啲 有呢啲底你會睇得舒服啲咁解

如果你剩係用我呢個post暫時講過嘅嘢去judge stoc cal有冇用

咁我只可以講你真係太天真

同埋我一開頭都講呢個post係introduction

我唔會亦都冇可能講到去LIBOR market model嗰啲位

我依家講嘅嘢只係basic 如果你再另外睇書讀深啲 有呢啲底你會睇得舒服啲咁解

Estimating volatility is already a huge problem

咪因為Black Scholes Model冇incorporate到stochastic volatility

現實implied volatility明明有smile有skew

但係BS Model冇處理過 佢係直接assume volatility係constant

咁LTCM會死得咁慘都好正常

同埋佢嘅死唔係更加突顯到呢堆嘢嘅重要性咩?

更加證明我地要認真處理呢啲stochastic model

而且啲model應該要愈黎愈貼近現實 咁先可以做到更加好嘅risk management

現實implied volatility明明有smile有skew

但係BS Model冇處理過 佢係直接assume volatility係constant

咁LTCM會死得咁慘都好正常

同埋佢嘅死唔係更加突顯到呢堆嘢嘅重要性咩?

更加證明我地要認真處理呢啲stochastic model

而且啲model應該要愈黎愈貼近現實 咁先可以做到更加好嘅risk management

冇人話要計implied volatility

不嬲cal個model嗰時都係當imp vol係known information

我地要做嘅係令我地嘅model盡量貼近個market

唔係點解會叫MTM Mark to market?

不嬲cal個model嗰時都係當imp vol係known information

我地要做嘅係令我地嘅model盡量貼近個market

唔係點解會叫MTM Mark to market?

Implied volatilities are calculated from option prices assuming the underlying follows the Black Scholes model.

We can also estimate the actual volatility statistically. There are pros and cons for hedging using implied vol or actual vol.

We can also estimate the actual volatility statistically. There are pros and cons for hedging using implied vol or actual vol.

4.) Girsanov Thoerem (Change of measure) & its application

Brief Intro to Multivariate Normal Distribution

(iv) Generating Normal R.V.s with correlation (Cholesky Decomposition)

喺我再講落去之前 我想大家由一個practical啲嘅角度去諗

我地一路以嚟揾到咁多close form pricing formula其實某程度上都係因為我地用緊一個最簡單嘅model (BS) 同處理緊比較簡單嘅derivatives

如果換轉係一隻有奇怪payoff嘅deriv 或者 一個更加複雜嘅model

其實係好難純粹靠stoc cal去寫低一個close form

而呢個時候 Monte Carlo Simulation就大派用場

個原理其實就係Law of large numbers (LLN)

當同一個experiment重複做好多好多次 咁sample mean就會converge to expected value (population mean)

而simulation就係base on呢個result

假設我地想simulate普通european call price

咁首先定咗一個constant "n" 先 (e.g. n = 100,000) 同埋我地用乜model先 為咗方便起見假設係用BS model先

跟住要做嘅嘢好簡單

首先generate n 條 stock price path 得到每條path嘅 S_T

然後就將每條path嘅discounted payoff, i.e. exp(-rT)*max(S_T - K,0) 計出黎

最尾將呢n個discounted payoff take average就會得到一個"estimated" call price

而理論上當n tends to +infinity, sim出黎嘅call price就會同用BS close form計出黎嘅call price一樣

點解會一樣? 因為本來call price就係expectation of discounted payoff (其實under risk-neutral pricing嘅話就所有deriv都係)

而simulation正正就係計緊sample mean

所以根據LLN 當n趨向無限我地就會得到返真正嘅expectation

(遲啲我真係開始講simulation就會講得詳細啲 所有proof同數都會留返個時先講

依家只係交待返個背景 等大家有足夠嘅background knowledge繼續睇落去)

咁大家諗下 如果我地做simulation一開始要generate stock price path嘅話

其實即係要將原本條SDE discretise擺落programme入面 (或者直接one-shoot由0 sim去 T, 但係下述嘅問題都係存在)

而咁樣做最大嘅問題就係我地應該點樣塞一條wiener process落個programme裡面?

大家睇完上半part應該都仲記得 (change of) Wiener process dW_t ~ N(0,dt)

所以我地其實可以當change of wiener process係一粒follow normal distribution嘅random number咁睇

因為咁 個問題就簡化到點樣generate一粒follow normal distribution嘅random number?

或者換個角度問就係我地用電腦可以點喺一個normal distribution入面拎一粒sample出黎?

( 詳細點樣generate容後再講 因為我想連埋variance reduction去講 咁樣個脈絡會完整啲 )

***IMPORTANT DISCLAIMER***

我知道一定會有人講 所以我自己利申曬先

用電腦gen出黎嘅所謂"random number"一定唔會係真正意義上嘅random

電腦default又好 你自己寫又好 其實都係靠一啲algorithm去gen呢啲數

當然粒seed可以真係random 但係通常電腦default都係用時間去做seed

所以呢啲pseudo-random number只係feels random

只要computing power夠勁就可以predict到一條pseudo-random number series嘅result

或者你可以將個algorithm寫到以現今嘅computing power根本冇可能recognise到究竟條series係咪random

咁你就可以老屈你gen緊嗰啲數係"random"嘅

但係真正嘅random都唔係冇辦法做到

大家可以參考以下numberphile嘅兩段片

兩段都係討論randomness 而且都講得好好

https://www.youtube.com/watch?v=SxP30euw3-0

https://www.youtube.com/watch?v=tP-Ipsat90c

***IMPORTANT DISCLAIMER***

咁假設我地真係寫到個programme 可以喺一個standard normal distribution裡面抽到任意咁多粒independent嘅sample出黎

i.e. 我地個programme generate到任意咁多粒independent嘅random number 而佢地全部follow N(0,1)

上面咁講係咪好長氣呢 所以通常我地會好似下面幅圖咁寫

where i.i.d. = independent and identically distributed

咁其實我地已經處理到n條互相冇correlation嘅wiener processes嘅simulation

但係當我地加咗correlation入去嗰n條processes入面 真正嘅問題就出現

上面我地一路都係講緊in general n粒R.V.s 嘅case

首先我地簡化少少先 剩係consider兩粒 R.V.s , i.e. X_1 and X_2

然後再assume埋 X_1 , X_2 ~ N(0,1)

而佢地係jointly follow Bivariate Normal Distribution (with correlation ρ)

有咗上面堆assumption之後 我地就可以開始問真正關鍵嘅問題

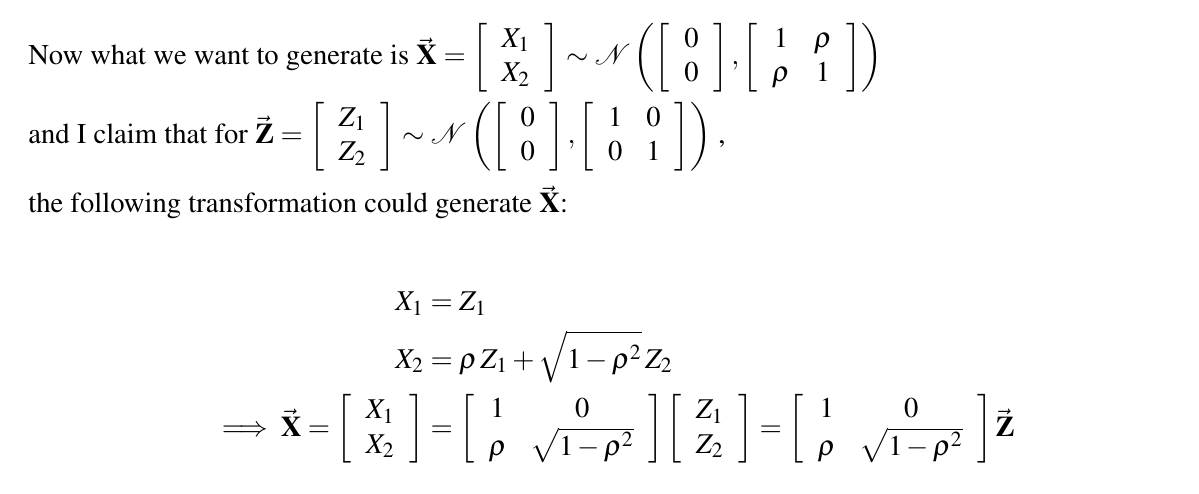

「究竟有冇辦法用 另外兩粒iid 嘅 standard normal R.V.s (i.e. Z_1 and Z_2) 去 generate到 X_1 同 X_2 出黎?」

換句話講即係問緊我地有冇辦法將個correlation structure塞入去 Z_1 , Z_2 入面令佢地變成 X_1 , X_2

點解我要特別強調用兩粒iid 嘅 R.V.s Z_1 , Z_2 去 generate X_1 同 X_2?

因為上面我地講咗我地係識點gen iid 嘅random number

如果我地有得apply一啲transformation落去Z_1同Z_2身上 令我地真係可以將個correlation structure塞入去

從而最後得到X_1同X_2 你話世界幾美好?

今次大家夠運啦 因為真係咁美好 有一個transformation係做到呢樣嘢 請睇下圖

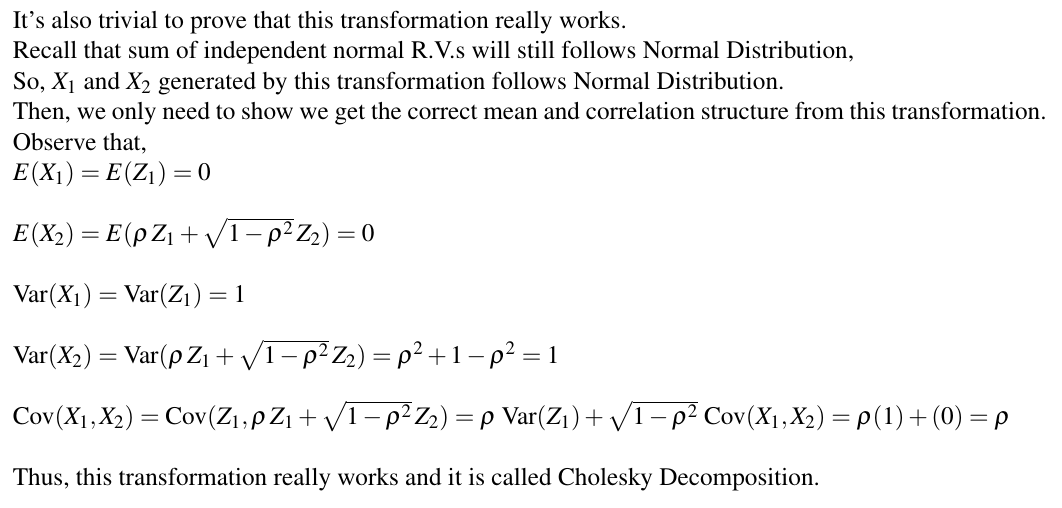

咁依家我claim佢work姐 佢係咪真係work先?

大家唔洗煩惱 寫個簡單嘅proof就可以證明呢個transformation真係work

而呢個transformation technique就係好出名嘅Cholesky Decomposition

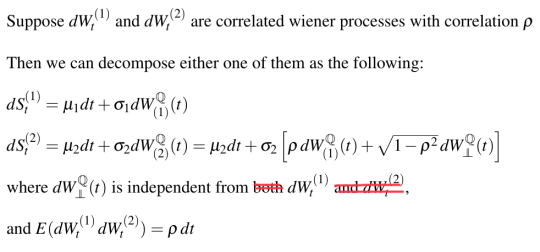

所以好naive咁諗 如果我地將本來啲X_1 , X_2 , Z_1 , Z_2轉曬做wiener processes

咁我地已經可以將兩條有correlation ρ嘅wiener processes decompose返做兩條independent嘅 wiener processes

實際嘅寫法就好似下圖咁 (想知點解咁寫就自己再睇書 我又爆字數)

Brief Intro to Multivariate Normal Distribution

(iv) Generating Normal R.V.s with correlation (Cholesky Decomposition)

喺我再講落去之前 我想大家由一個practical啲嘅角度去諗

我地一路以嚟揾到咁多close form pricing formula其實某程度上都係因為我地用緊一個最簡單嘅model (BS) 同處理緊比較簡單嘅derivatives

如果換轉係一隻有奇怪payoff嘅deriv 或者 一個更加複雜嘅model

其實係好難純粹靠stoc cal去寫低一個close form

而呢個時候 Monte Carlo Simulation就大派用場

個原理其實就係Law of large numbers (LLN)

當同一個experiment重複做好多好多次 咁sample mean就會converge to expected value (population mean)

而simulation就係base on呢個result

假設我地想simulate普通european call price

咁首先定咗一個constant "n" 先 (e.g. n = 100,000) 同埋我地用乜model先 為咗方便起見假設係用BS model先

跟住要做嘅嘢好簡單

首先generate n 條 stock price path 得到每條path嘅 S_T

然後就將每條path嘅discounted payoff, i.e. exp(-rT)*max(S_T - K,0) 計出黎

最尾將呢n個discounted payoff take average就會得到一個"estimated" call price

而理論上當n tends to +infinity, sim出黎嘅call price就會同用BS close form計出黎嘅call price一樣

點解會一樣? 因為本來call price就係expectation of discounted payoff (其實under risk-neutral pricing嘅話就所有deriv都係)

而simulation正正就係計緊sample mean

所以根據LLN 當n趨向無限我地就會得到返真正嘅expectation

(遲啲我真係開始講simulation就會講得詳細啲 所有proof同數都會留返個時先講

依家只係交待返個背景 等大家有足夠嘅background knowledge繼續睇落去)

咁大家諗下 如果我地做simulation一開始要generate stock price path嘅話

其實即係要將原本條SDE discretise擺落programme入面 (或者直接one-shoot由0 sim去 T, 但係下述嘅問題都係存在)

而咁樣做最大嘅問題就係我地應該點樣塞一條wiener process落個programme裡面?

大家睇完上半part應該都仲記得 (change of) Wiener process dW_t ~ N(0,dt)

所以我地其實可以當change of wiener process係一粒follow normal distribution嘅random number咁睇

因為咁 個問題就簡化到點樣generate一粒follow normal distribution嘅random number?

或者換個角度問就係我地用電腦可以點喺一個normal distribution入面拎一粒sample出黎?

( 詳細點樣generate容後再講 因為我想連埋variance reduction去講 咁樣個脈絡會完整啲 )

***IMPORTANT DISCLAIMER***

我知道一定會有人講 所以我自己利申曬先

用電腦gen出黎嘅所謂"random number"一定唔會係真正意義上嘅random

電腦default又好 你自己寫又好 其實都係靠一啲algorithm去gen呢啲數

當然粒seed可以真係random 但係通常電腦default都係用時間去做seed

所以呢啲pseudo-random number只係feels random

只要computing power夠勁就可以predict到一條pseudo-random number series嘅result

或者你可以將個algorithm寫到以現今嘅computing power根本冇可能recognise到究竟條series係咪random

咁你就可以老屈你gen緊嗰啲數係"random"嘅

但係真正嘅random都唔係冇辦法做到

大家可以參考以下numberphile嘅兩段片

兩段都係討論randomness 而且都講得好好

https://www.youtube.com/watch?v=SxP30euw3-0

https://www.youtube.com/watch?v=tP-Ipsat90c

***IMPORTANT DISCLAIMER***

咁假設我地真係寫到個programme 可以喺一個standard normal distribution裡面抽到任意咁多粒independent嘅sample出黎

i.e. 我地個programme generate到任意咁多粒independent嘅random number 而佢地全部follow N(0,1)

上面咁講係咪好長氣呢 所以通常我地會好似下面幅圖咁寫

where i.i.d. = independent and identically distributed

咁其實我地已經處理到n條互相冇correlation嘅wiener processes嘅simulation

但係當我地加咗correlation入去嗰n條processes入面 真正嘅問題就出現

上面我地一路都係講緊in general n粒R.V.s 嘅case

首先我地簡化少少先 剩係consider兩粒 R.V.s , i.e. X_1 and X_2

然後再assume埋 X_1 , X_2 ~ N(0,1)

而佢地係jointly follow Bivariate Normal Distribution (with correlation ρ)

有咗上面堆assumption之後 我地就可以開始問真正關鍵嘅問題

「究竟有冇辦法用 另外兩粒iid 嘅 standard normal R.V.s (i.e. Z_1 and Z_2) 去 generate到 X_1 同 X_2 出黎?」

換句話講即係問緊我地有冇辦法將個correlation structure塞入去 Z_1 , Z_2 入面令佢地變成 X_1 , X_2

點解我要特別強調用兩粒iid 嘅 R.V.s Z_1 , Z_2 去 generate X_1 同 X_2?

因為上面我地講咗我地係識點gen iid 嘅random number

如果我地有得apply一啲transformation落去Z_1同Z_2身上 令我地真係可以將個correlation structure塞入去

從而最後得到X_1同X_2 你話世界幾美好?

今次大家夠運啦 因為真係咁美好 有一個transformation係做到呢樣嘢 請睇下圖

咁依家我claim佢work姐 佢係咪真係work先?

大家唔洗煩惱 寫個簡單嘅proof就可以證明呢個transformation真係work

而呢個transformation technique就係好出名嘅Cholesky Decomposition

所以好naive咁諗 如果我地將本來啲X_1 , X_2 , Z_1 , Z_2轉曬做wiener processes

咁我地已經可以將兩條有correlation ρ嘅wiener processes decompose返做兩條independent嘅 wiener processes

實際嘅寫法就好似下圖咁 (想知點解咁寫就自己再睇書 我又爆字數

)上半part下半part都係爆字數 但係總算講完

我知Cholesky Decomposition仲有好多嘢冇講

不過大家暫時知道2條Wiener processes點decompose就夠

因為我之後講嗰兩個example都剩係牽涉兩條processes 所以暫時夠用

遲啲真係講simulation我就會奉上完整版嘅CD

下次再出應該要6/3之後 唔經唔覺又midterm了

跟住會講exchange option先

但係總算講完我知Cholesky Decomposition仲有好多嘢冇講

不過大家暫時知道2條Wiener processes點decompose就夠

因為我之後講嗰兩個example都剩係牽涉兩條processes 所以暫時夠用

遲啲真係講simulation我就會奉上完整版嘅CD

下次再出應該要6/3之後 唔經唔覺又midterm了

跟住會講exchange option先

啱啱發現自己痴撚咗線打錯嘢

#540最尾幅圖應該係咁樣先啱

#540最尾幅圖應該係咁樣先啱

By the way, in page20 you mentioned bond options being exotic. But I thought exotic means some kinda path dependent products as opposed to vanilla products?

I think in the current market, the word “exotic” indeed refers to products with some kind of path dependent payoff

But in a broader sense, it could also refer to uncommon products traded in the market in contrast to vanilla options

But in a broader sense, it could also refer to uncommon products traded in the market in contrast to vanilla options

Indeed anything that’s not vanilla are called exotic. I’m just not sure if an European call on a bond is exotic. Coz the payoff of an European call is considered vanilla.

Oh I see your point

Maybe the best way is not to classify it

Maybe the best way is not to classify it

And usually exotic products are priced by Monte Carlo simulation.

By the way do you have a chat group? Telegram is not working I think.

By the way do you have a chat group? Telegram is not working I think.