Introduction to Stochastic Calculus & Application in Finance

宇智波月巴

674 回覆

359 Like

8 Dislike

講埋markov martingale 嘛

利申: 行家

利申: 行家

連probability都無點學stochastic calculus

留名

下年minor要學

下年minor要學

有啲用ms word有啲又用latex Beamer class嘅

Btw數撚留名

Btw數撚留名

算撚數

連狗淨係識數浪畫圖

連狗淨係識數浪畫圖

留名學野 ,其實香港有冇data analysis 呢行

,其實香港有冇data analysis 呢行

,其實香港有冇data analysis 呢行認真 樓主如果用呢種文筆出書 應該會幾好賺

2b.) Ito's lemma and isometry

Ito's lemma同isometry可以話係令Stochastic calculus真正workable嘅神兵利器

之後好多result都需要用到呢條lemma同埋isometry

所以呢一part係非常非常重要嘅foundation!!!

之不過係真正打大佬之前

我地其實仲有兩個concept要build up --- 佢地分別就係Information (F) 同 Martingale

----------------------------------

(a). Information/Filtration (or in rigorous term "σ-field")

下圖係"比較formal"嘅definition

大家都係唔洗比啲鬼畫符嚇親

我地首先簡化咗個情況先 假設我地依家有n個time point

然後我地假設埋每個timepoint嘅stock price係 S(t_0) = 100, S(t_1) = 99.5 ,...., S(t_(n-1)) = 97

如果time now = t_(n-1) 咁information generated by S at time = t_(n-1)就包含上面所有野

個concept其實就類似係咁

(其實唔止包含咁少野 有興趣知多啲可以睇埋下面optional個段)

跟住我地又黎abuse notation

正常黎講我地只可以話一啲event/set係喺information/filtration入面

但因為stochastic variable個domain其實係sample space(一堆event)

所以我地就直接abuse notation(好似上圖咁)

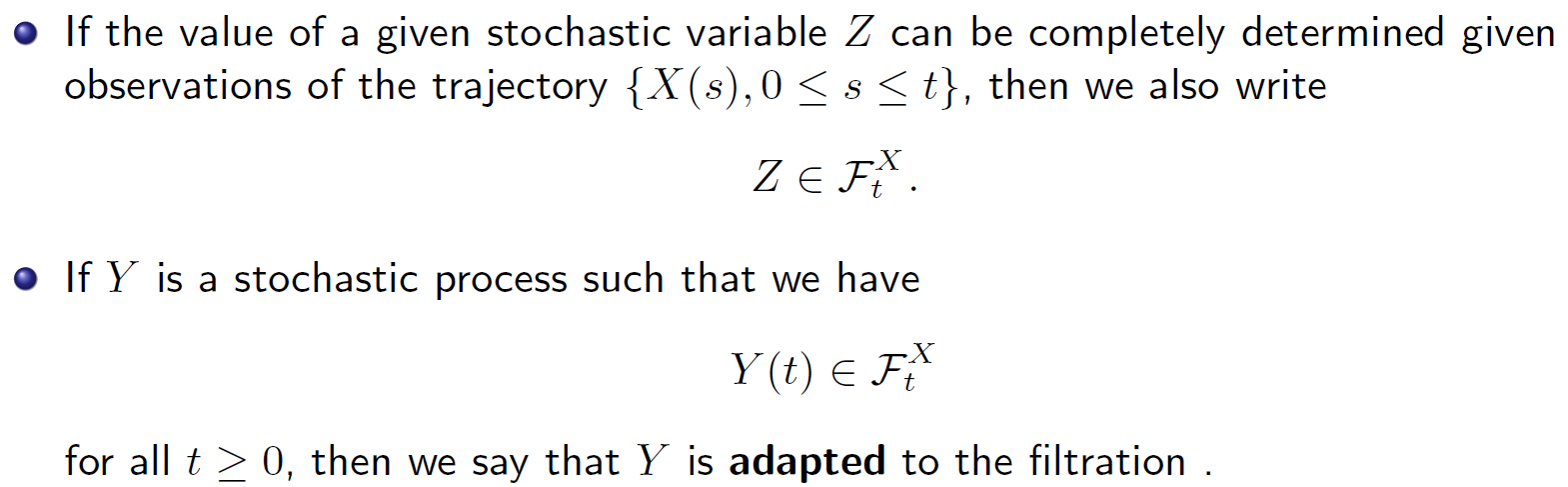

如果given information up to time t, Z可以完全determine到嘅話

我地就話 "Z is adapted to the filtration"

----------------------------------

(b). Martingale

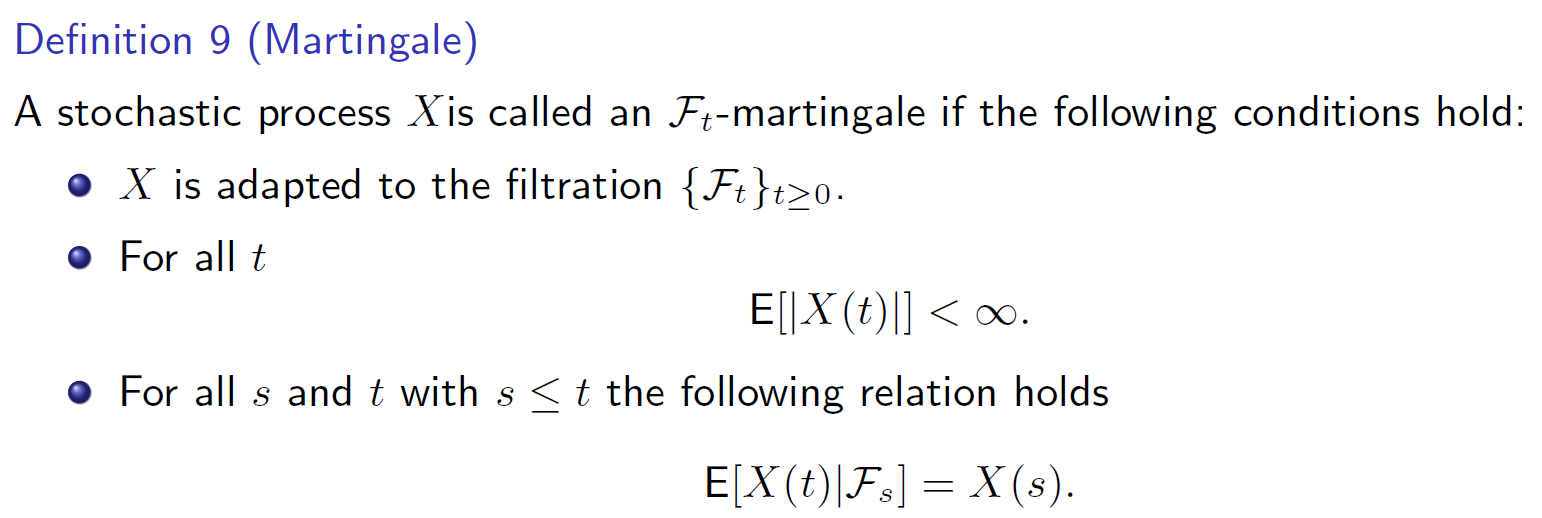

下圖係formal definition

其實最重要嘅property係第三點

如果given information up to time s (s<=t)

咁呢個stochastic variable X(t)嘅conditional expectation 只會係X(s)

In other words, the expectation is only up to current knowledge

另一種講法就係當呢個X係martingale 咁樣先會係fair game

點解係fair game?

大家試想下 如果個conditional expectation係細過X(s)

咁即係代表in long run, 你係會不停輸錢 (The technical term is supermartingale)

而相反X(s) > E[X(t)|F_s] => in long run不停贏錢 (The technical term is submartingale)

只有兩者相等先會係fair game

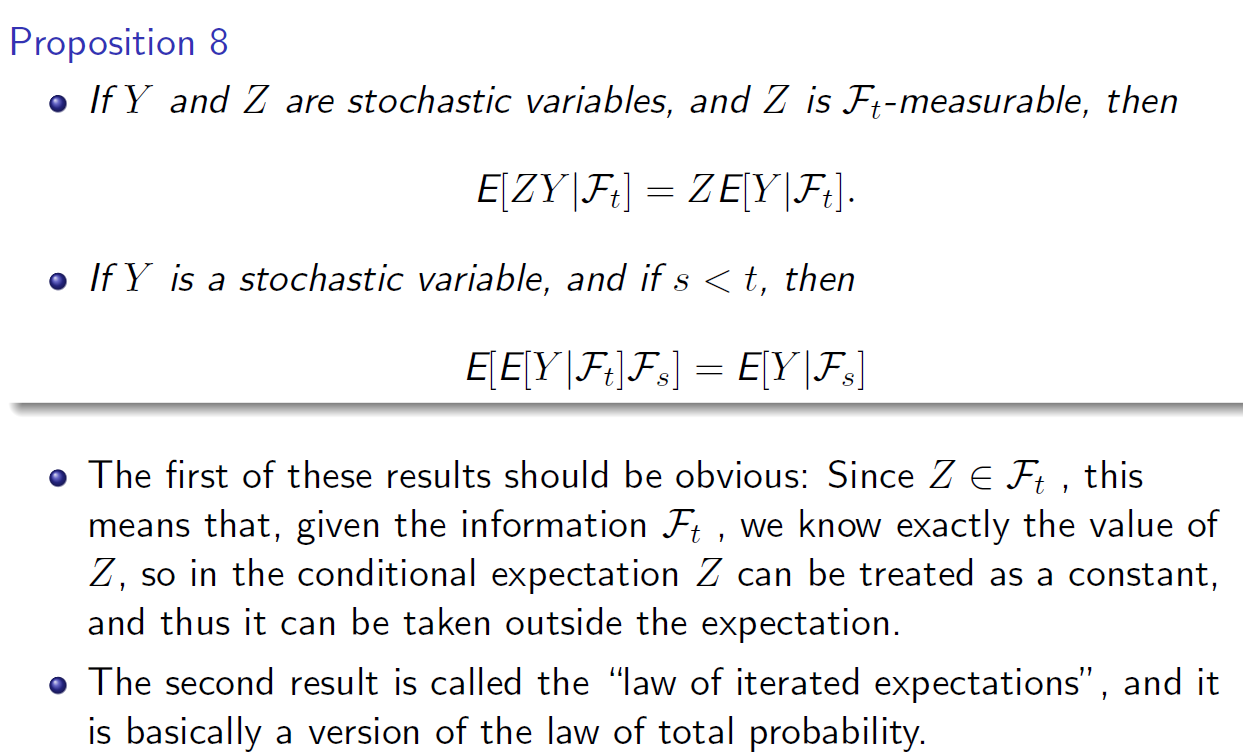

下圖係兩個好trivial嘅related result

----------------------------------

(c). Ito's isometry

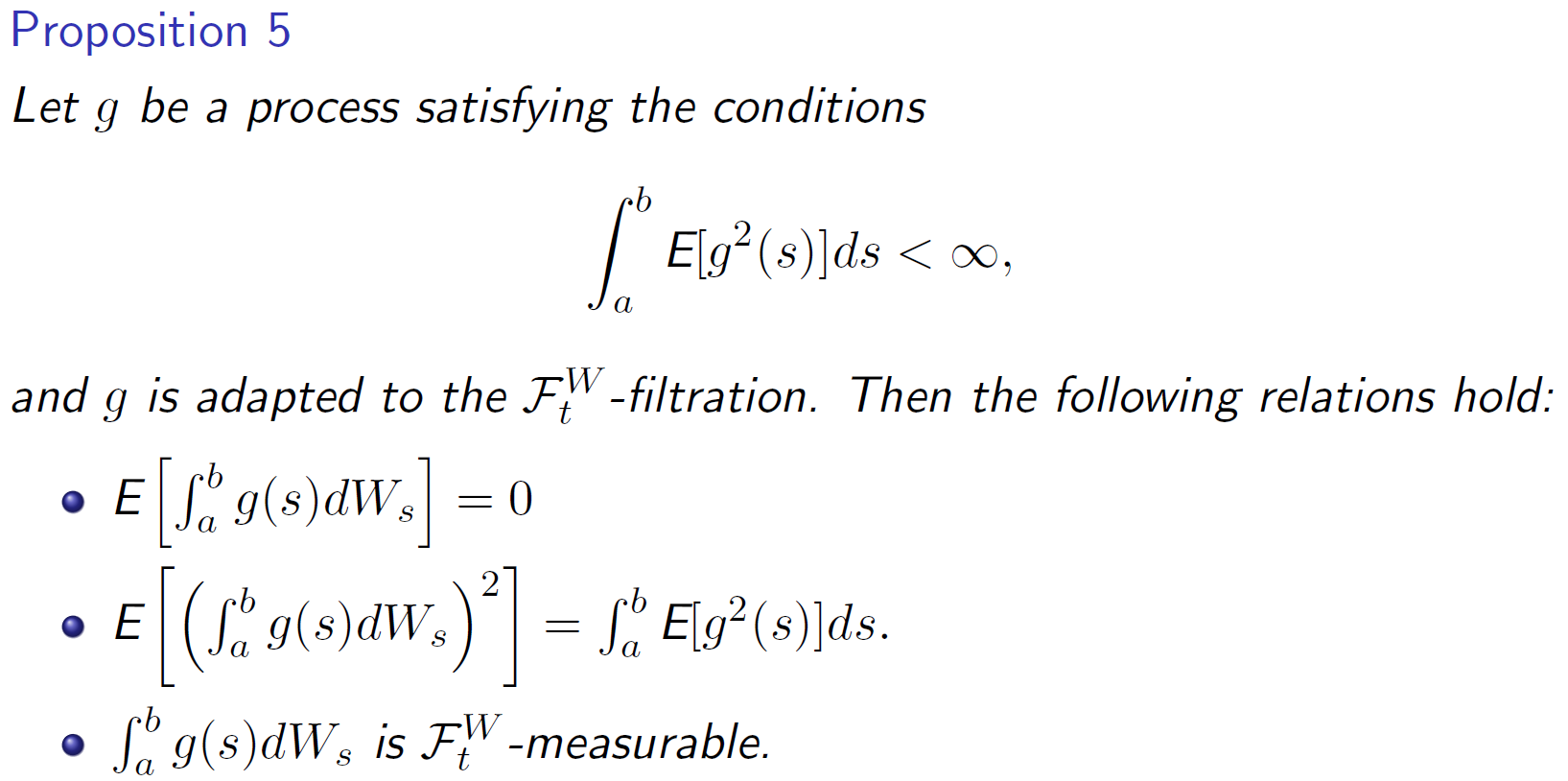

上圖就係大家期待而久嘅ito's isometry

點解ito's isometry咁有用? 就係因為佢話左比我聽expectation of stochastic integral可以點計

大家首先諗下普通integral係點樣嘅先 最後面個"ds"嘅"s"應該係deterministic嘅

但係依家stochastic integral顧名思義 "dW(s)"嘅"W(s)"係stochastic(random)嘅

所以依靠平時計riemann integral (or lebesgue integral)嘅方法係冇任何幫助

不過既然係random嘅野 咁用返我地學random variable嘅logic

我地照樣可以搵呢樣野嘅mean (E) 同 variance (VAR)係咩

而ito's isometry就已經直接話左比我地聽呢兩樣野分別點計

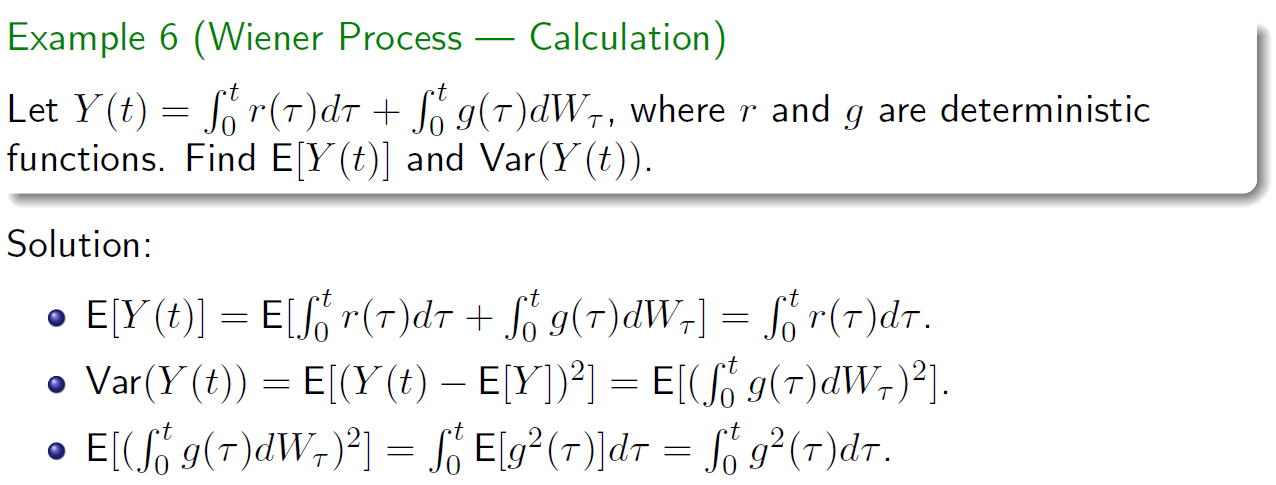

比個好簡單嘅例子大家:

(希望大家follow到example嘅steps 唔明可以隨時問 )

)

相信醒目嘅朋友已經即刻知道呢個isometry有幾勁

如果我地知道E(Y)同Var(Y(t)) 加埋dW(t) follows Normal 呢個property

我地可以rewrite Y as the following:

咁樣就可以方便我地去用電腦simulate呢個Y (因為我地知道點樣sim standard normal嘅variable)

-----------------------------------

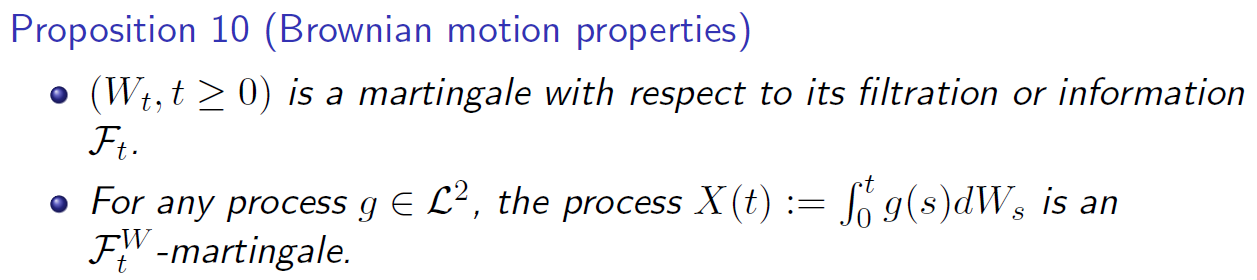

(d). Application of Ito's isometry

Ito's isometry 對martingale有兩個重要嘅result 請睇下圖

1.) Wiener process係martingale (其實佢仲係markov process添 因為無論你知道幾多history都好 都只係最latest嘅information對你有用)

2.) 呢個result話咗比我聽 如果一個stochastic process X要係martingale 咁佢一定要冇drift term

----------------------------------

打住咁多先 ito's lemma下個cm講 我唔夠位了

Ito's lemma同isometry可以話係令Stochastic calculus真正workable嘅神兵利器

之後好多result都需要用到呢條lemma同埋isometry

所以呢一part係非常非常重要嘅foundation!!!

之不過係真正打大佬之前

我地其實仲有兩個concept要build up --- 佢地分別就係Information (F) 同 Martingale

----------------------------------

(a). Information/Filtration (or in rigorous term "σ-field")

下圖係"比較formal"嘅definition

大家都係唔洗比啲鬼畫符嚇親

我地首先簡化咗個情況先 假設我地依家有n個time point

然後我地假設埋每個timepoint嘅stock price係 S(t_0) = 100, S(t_1) = 99.5 ,...., S(t_(n-1)) = 97

如果time now = t_(n-1) 咁information generated by S at time = t_(n-1)就包含上面所有野

個concept其實就類似係咁

(其實唔止包含咁少野 有興趣知多啲可以睇埋下面optional個段)

跟住我地又黎abuse notation

正常黎講我地只可以話一啲event/set係喺information/filtration入面

但因為stochastic variable個domain其實係sample space(一堆event)

所以我地就直接abuse notation(好似上圖咁)

如果given information up to time t, Z可以完全determine到嘅話

我地就話 "Z is adapted to the filtration"

[Content below is optional to readers]

點解我會話呢個只係"比較formal"嘅definition?

因為information/filtration其實即係一個sample space嘅σ-field

咩係σ-field? 大家有讀過probability嘅話應該都會見過呢三兄弟 (Ω,F,P) 中間嘅F就係σ-field

而σ-field本身就已經有一個非常formal嘅definition (contains ∅ and Ω, close under complement, close under countable union)

我假設大家睇得呢段野都有學過咩叫σ-field啦(想學多啲就睇下measure theory)

依家你可以幻想下我地model緊stock price嘅movement

一個簡單啲嘅情況係想像有n個discrete嘅time point

咁係t = 1嘅時候 我地嘅information 其實就係類似係 F1 = {∅,{S_0},{S_1},{S_1嘅complement},Ω}

where {S_n} = the event that stock price at time n equals to S_n

當然呢個非常非常informal嘅寫法 不過大家可以見到其實呢個information set即係σ-field

而F1係會包含係F2入面 如此類推

(In other words, information/filtration is essentially a collection of subsets of σ-field)

----------------------------------

(b). Martingale

下圖係formal definition

其實最重要嘅property係第三點

如果given information up to time s (s<=t)

咁呢個stochastic variable X(t)嘅conditional expectation 只會係X(s)

In other words, the expectation is only up to current knowledge

另一種講法就係當呢個X係martingale 咁樣先會係fair game

點解係fair game?

大家試想下 如果個conditional expectation係細過X(s)

咁即係代表in long run, 你係會不停輸錢 (The technical term is supermartingale)

而相反X(s) > E[X(t)|F_s] => in long run不停贏錢 (The technical term is submartingale)

只有兩者相等先會係fair game

下圖係兩個好trivial嘅related result

----------------------------------

(c). Ito's isometry

上圖就係大家期待而久嘅ito's isometry

點解ito's isometry咁有用? 就係因為佢話左比我聽expectation of stochastic integral可以點計

[Content below is optional to readers]

第一句嘅assumption其實即係話

大家首先諗下普通integral係點樣嘅先 最後面個"ds"嘅"s"應該係deterministic嘅

但係依家stochastic integral顧名思義 "dW(s)"嘅"W(s)"係stochastic(random)嘅

所以依靠平時計riemann integral (or lebesgue integral)嘅方法係冇任何幫助

不過既然係random嘅野 咁用返我地學random variable嘅logic

我地照樣可以搵呢樣野嘅mean (E) 同 variance (VAR)係咩

而ito's isometry就已經直接話左比我地聽呢兩樣野分別點計

比個好簡單嘅例子大家:

(希望大家follow到example嘅steps 唔明可以隨時問

)相信醒目嘅朋友已經即刻知道呢個isometry有幾勁

如果我地知道E(Y)同Var(Y(t)) 加埋dW(t) follows Normal 呢個property

我地可以rewrite Y as the following:

咁樣就可以方便我地去用電腦simulate呢個Y

(因為我地知道點樣sim standard normal嘅variable)-----------------------------------

(d). Application of Ito's isometry

Ito's isometry 對martingale有兩個重要嘅result 請睇下圖

1.) Wiener process係martingale (其實佢仲係markov process添 因為無論你知道幾多history都好 都只係最latest嘅information對你有用)

2.) 呢個result話咗比我聽 如果一個stochastic process X要係martingale 咁佢一定要冇drift term

----------------------------------

打住咁多先 ito's lemma下個cm講 我唔夠位了

gg我唔識呢堆野

RMSC嘅course冇教到咁深

RMSC嘅course冇教到咁深

因為有啲野我係直接由notes (pdf) crop過黎 懶得再係word打一次

懶得再係word打一次難到仆街

This is the magic of abusing notation

你要記得我由頭到尾都冇話過佢d到

我只係將∆t->0

然後用dW(t) 代替 W(t+∆t) - W(t), same for dX(t)

你要記得我由頭到尾都冇話過佢d到

我只係將∆t->0

然後用dW(t) 代替 W(t+∆t) - W(t), same for dX(t)

我講ito's lemma嘅時候就會一次過處理曬呢堆野

屌,HKU 啲 stochastic 講咁深入既

垃圾 CU 教到 markov chain , continuous markov chain, birth and death process 就算

就算 ODE 都係輕輕帶過,連 PDE 都無講過

垃圾 CU 教到 markov chain , continuous markov chain, birth and death process 就算

就算 ODE 都係輕輕帶過,連 PDE 都無講過

stochastic process同stochastic calculus唔同架喎

屌,唔小心將R4005 同 Stat3007 撈亂左