Leveraged ETF 討論區 (13)

Outliers

1001 回覆

4 Like

0 Dislike

唔睇市 +1 LM

想問有人研究fas

成份股主要包括巴郡、世界頂尖嘅銀行、ibank,佢地嘅質素都相當好,而且加息對銀行股都有利

不過FAS距離上一個低位已經升咗27%,而家先放TQQQ轉去FAS小心左一巴右一巴

不過FAS距離上一個低位已經升咗27%,而家先放TQQQ轉去FAS小心左一巴右一巴

上一個炒加息週期已經出入左一轉 當時係到提過

而家都priced in左 暫時冇興趣

而家都priced in左 暫時冇興趣

Out巴我見google doc都係咁寫

8.73% to 17.91%好似唔係3x to 3x,篇文寫法可能令人有歧義,不過都睇到少少

總結可能會清晰啲

睇圖應該最清楚

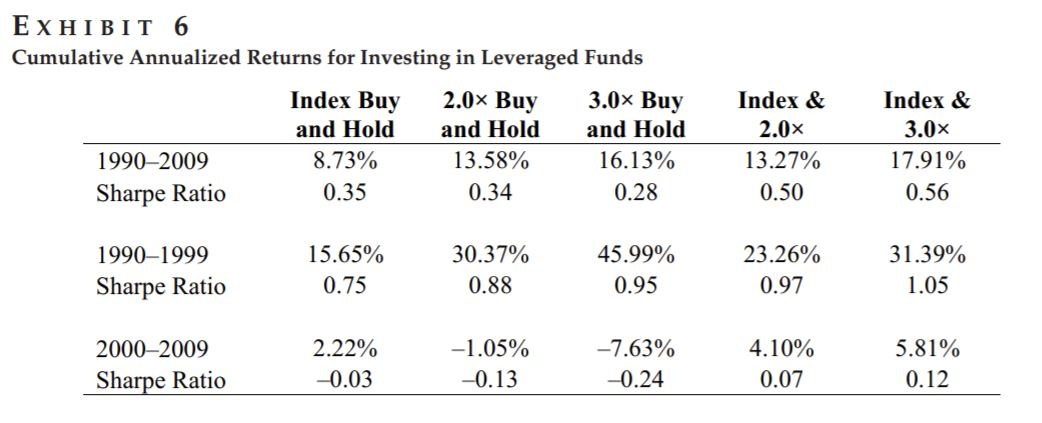

https://sci-hub.se/https://doi.org/10.3905/jii.2011.1.4.066

High Volatility對LETF回報嘅負面影響大家都知。以上依篇論文就探討可唔可以避開high volatility嘅時間,淨係揀low volatility嘅時間先投資LETF。

咁點樣知道將來嘅volatility係高定低呢?作者用VIX去預測。因為VIX反映投資者對S&P 500未來30天的預期年化波動率,所以策略就係「等VIX跌穿20先買LETF」,結果咁簡單嘅策略可以將年化回報率由8.73%提高到17.91%,Sharpe ratio都顯著提高咗。

8.73% to 17.91%好似唔係3x to 3x,篇文寫法可能令人有歧義,不過都睇到少少

For the overall time period, the cumulative annualized return is increased from 8.73% to as much as 17.91% for a 3.0× fund.This strategy outperforms the “buy and hold on for dear life” strategy for leveraged funds as well, although not as dramatically in terms of absolute returns only.

總結可能會清晰啲

Over the past 20 years, moving out of index funds and into 2.0× or 3.0× levered funds based on this idea could have increased the cumulative annualized return from 8.73% to as much as 17.91% while substantially increasing the Sharpe ratio as well.

睇圖應該最清楚

premarket 果斷120狠掃ed

今日直接唔睇算

咁岩啦,20年3月TLT見頂計,而加都跌左一年零九個月

差唔多到底

差唔多到底

總之玩portfo 就係鬥堅持,看誰可以喊到最後

又係喎,用返3x buy and hold嚟比較先啱

宜家係減買債?

唔係收水>加息>縮表咁去?

唔係收水>加息>縮表咁去?

縮減買債 -> 加息 -> 縮表

多左縮表

現貨溝咗一注tqqq 信者得救

信者得救

信者得救