多倫多生活討論區 105 Happy Canada day

唔上吾落

1001 回覆

13 Like

16 Dislike

點解?

新移民大家都黎左2-3年

contribution room又唔係多

慳稅效果有限

我認為等到儲多啲room

等到收入更多先一次過用

慳稅效果會更好

contribution room又唔係多

慳稅效果有限

我認為等到儲多啲room

等到收入更多先一次過用

慳稅效果會更好

有啲人係郊外揸開車慣咗少行人 一見冇車走直接踩油右轉

Frd 搭frd 搭frd 搭frd

咁講又啱喎!

依家右轉一定要睇清楚有冇單車之類。有啲ebike可以快到癲。

咁多社交媒體仲驚識唔到朋友?事在人為啫

大公司會match RRSP ,逼住供

首先要有朋友

It depends on the type of RRSP matching.

What Is RRSP Matching?

RRSP matching is when your employer has a group RRSP that you can join. When you contribute to the RRSP, your employer will either contribute to the plan or match your contributions. (Yes, there is a difference.) It’s a way to get extra money for your RRSP without you having to contribute said amount from your own money.

Is There a Difference Between RRSP Matching and Group RRSPs?

Before we get into how RRSP matching works, we need to define the difference between group RRSPs and RRSP matching.

A group RRSP is a program offered by an employer and usually managed by an outside firm like a bank or an insurance company. If your company has one, you’ll be told about it by the HR department (likely during your onboarding process). In some cases, you may have to wait for your probationary period to end before you can join, but in other cases, if you negotiate, you can join as soon as you start your new role.

RRSP matching can be an option as a part of a group RRSP, but it’s not automatically included. That’s because not all group RRSPs have a matching component. Some do, some don’t, but if RRSP matching is available, it can only be a feature of a group RRSP and not an individual one.

How Does Employer RRSP Matching Work?

Let’s say your company offers a group RRSP with employer matching. Depending on the structure of the group RRSP in question, The employer matching may present itself in two typical varieties. One option is match-for-match contributions. In this example you contribute 5% of your salary, the company matches it with another 5%.

Here’s how that math breaks down using an annual salary of $80,000:

Your RRSP contribution: $80,000 x 0.05 = $4,000

Employer matching (full 5%) = $4,000

Total = $8,000

The other common option is incentive matching. That’s when the company incentivizes you to contribute a certain percentage of your salary with the promise of matching your contributions to a certain stated percentage as well. So when you contribute 5%, the company will match it with an additional 3% or 4%.

Using the same annual salary of $80,000:

Your RRSP contribution: $80,000 x 0.05 = $4,000

Employer matching (3%) = $2,400

Total = $6,400

The main advantage of a group RRSP, especially one that offers matching, is the free money you get towards your retirement.

That’s a lot of extra money for minimal effort on your part.

The second benefit of contributing to a group RRSP is the ease. You sign up for it, determine how much you want to contribute per paycheque and you don’t have to think about it again. Out of sight, out of mind.

As with individual RRSP contributions, employer contributions are tax deductible and reduce your taxable income. This does offset the fact that there might be tax implications, as employer contributions may be considered income and will be reflected as such on your T4 form.

However, there are a couple disadvantages to contributing to a group RRSP. One is you don’t have much freedom to choose your investments as you would with an individual plan. The company plan is managed by an outside financial institution, so we recommend reading any reports, plan documentation and general fine print to see what kind of fees you may be paying, to stay informed about your exposure to risk and other details of the investment plan.

Another con, but one that is easy to manage, is the risk of over-contributing to both your RRSP plans. However, just because you are contributing to a company RRSP, doesn’t mean you still can’t have a personal plan.

If you have both a personal and a company plan, keep an eye on how much you’re contributing each year as employer contributions count towards your overall contribution room as an individual. Excess contributions are taxed at 1% per month over your lifetime over-contribution limit. Still, it’s easy to find out how much room you have in your RRSP plans on your annual tax return.

What Is RRSP Matching?

RRSP matching is when your employer has a group RRSP that you can join. When you contribute to the RRSP, your employer will either contribute to the plan or match your contributions. (Yes, there is a difference.) It’s a way to get extra money for your RRSP without you having to contribute said amount from your own money.

Is There a Difference Between RRSP Matching and Group RRSPs?

Before we get into how RRSP matching works, we need to define the difference between group RRSPs and RRSP matching.

A group RRSP is a program offered by an employer and usually managed by an outside firm like a bank or an insurance company. If your company has one, you’ll be told about it by the HR department (likely during your onboarding process). In some cases, you may have to wait for your probationary period to end before you can join, but in other cases, if you negotiate, you can join as soon as you start your new role.

RRSP matching can be an option as a part of a group RRSP, but it’s not automatically included. That’s because not all group RRSPs have a matching component. Some do, some don’t, but if RRSP matching is available, it can only be a feature of a group RRSP and not an individual one.

How Does Employer RRSP Matching Work?

Let’s say your company offers a group RRSP with employer matching. Depending on the structure of the group RRSP in question, The employer matching may present itself in two typical varieties. One option is match-for-match contributions. In this example you contribute 5% of your salary, the company matches it with another 5%.

Here’s how that math breaks down using an annual salary of $80,000:

Your RRSP contribution: $80,000 x 0.05 = $4,000

Employer matching (full 5%) = $4,000

Total = $8,000

The other common option is incentive matching. That’s when the company incentivizes you to contribute a certain percentage of your salary with the promise of matching your contributions to a certain stated percentage as well. So when you contribute 5%, the company will match it with an additional 3% or 4%.

Using the same annual salary of $80,000:

Your RRSP contribution: $80,000 x 0.05 = $4,000

Employer matching (3%) = $2,400

Total = $6,400

The main advantage of a group RRSP, especially one that offers matching, is the free money you get towards your retirement.

That’s a lot of extra money for minimal effort on your part.

The second benefit of contributing to a group RRSP is the ease. You sign up for it, determine how much you want to contribute per paycheque and you don’t have to think about it again. Out of sight, out of mind.

As with individual RRSP contributions, employer contributions are tax deductible and reduce your taxable income. This does offset the fact that there might be tax implications, as employer contributions may be considered income and will be reflected as such on your T4 form.

However, there are a couple disadvantages to contributing to a group RRSP. One is you don’t have much freedom to choose your investments as you would with an individual plan. The company plan is managed by an outside financial institution, so we recommend reading any reports, plan documentation and general fine print to see what kind of fees you may be paying, to stay informed about your exposure to risk and other details of the investment plan.

Another con, but one that is easy to manage, is the risk of over-contributing to both your RRSP plans. However, just because you are contributing to a company RRSP, doesn’t mean you still can’t have a personal plan.

If you have both a personal and a company plan, keep an eye on how much you’re contributing each year as employer contributions count towards your overall contribution room as an individual. Excess contributions are taxed at 1% per month over your lifetime over-contribution limit. Still, it’s easy to find out how much room you have in your RRSP plans on your annual tax return.

睇歐國杯又好 nba好 羽毛球都好 好多鬼佬好後生就生仔

反而香港人真係好少成立家庭

反而香港人真係好少成立家庭

不如試下參與啲你本身興趣嘅event黎識人

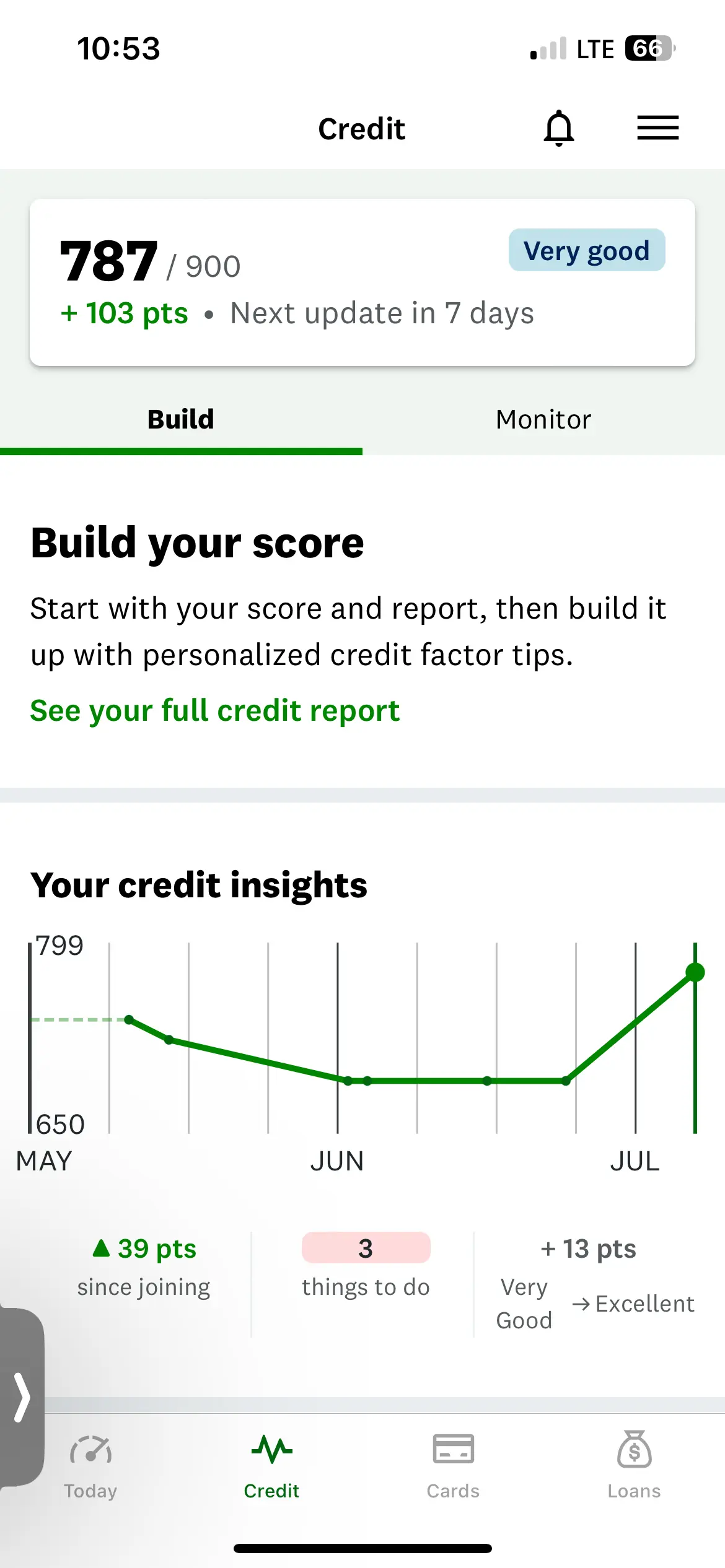

Credit score 唔知做乜大上大落

6月果陣730跌到落684

7月就684升返上787

6月果陣730跌到落684

7月就684升返上787

嚟到大家都做黎生,放假都休息下算,邊有精力join咁多興趣班

1. 邏輯上,交嗰下有效就得

2. 呢度政府效率咁慢,唔收貨可能拖好耐先同你講仲唔知有無得補,咁擔心不如預多一期糧畀佢計。

2. 呢度政府效率咁慢,唔收貨可能拖好耐先同你講仲唔知有無得補,咁擔心不如預多一期糧畀佢計。

Ok好唔該哂師兄

我交都多一個月ge pay stub 穩陣d

大原則 所有嘢有咁保守得咁保守,你比佢打一次回頭又有排等

另外可以查定過去10年/18歲後,有stay過半年or above嘅地方點拎良民證,佢會叫你比

另外可以查定過去10年/18歲後,有stay過半年or above嘅地方點拎良民證,佢會叫你比

有冇人用virgin plus呢個月無啦啦加咗價?

可唔可以打去cs 叫佢減返?

可唔可以打去cs 叫佢減返?