加拿大理財討論區

馬上風

1001 回覆

58 Like

5 Dislike

所有海外資產成本超過10萬蚊就要報

開返幾間公司,寫老母名

10 萬界限係一年一年計。譬如第一年低過十萬,就唔使報,第二年高過十萬,就要報。第三年又低過十萬又唔使報。 不過如第三係幾接近十萬既話,穩陣啲都係報埋佢。 但係如果差太遠而將來都無乜機會再高過十萬,咁就唔使報嘞。

如果香港有同父母嘅聯名戶口係咪都會100%當係我個人嘅海外資產?

定係有冇話其實得1/3先會係屬於自己?

定係有冇話其實得1/3先會係屬於自己?

唔該uncle

有得比你填joint寫%

想問下香港最後一份糧喺我到埗加拿大後先出返俾我

咁我嗰舊數洗唔洗報稅?

咁我嗰舊數洗唔洗報稅?

Check 唔到

No

請問我有隻us corp bond買左幾年,將會係我入境兩個月後到maturity 第一年唔使報海外資產係咪即使超過10萬CAD都唔使報?

第一年唔使報海外資產係咪即使超過10萬CAD都唔使報?

第一年唔使報海外資產係咪即使超過10萬CAD都唔使報?

存款如果加埋其他海外資產超過10萬

Yes

銀行收息係報foreign income

保險就唔清楚

Yes

銀行收息係報foreign income

保險就唔清楚

第一年係唔使報海外資產

但注意入境嗰日隻bond個價係你嘅成本價

到mature嗰陣要計返capital gain/loss

但注意入境嗰日隻bond個價係你嘅成本價

到mature嗰陣要計返capital gain/loss

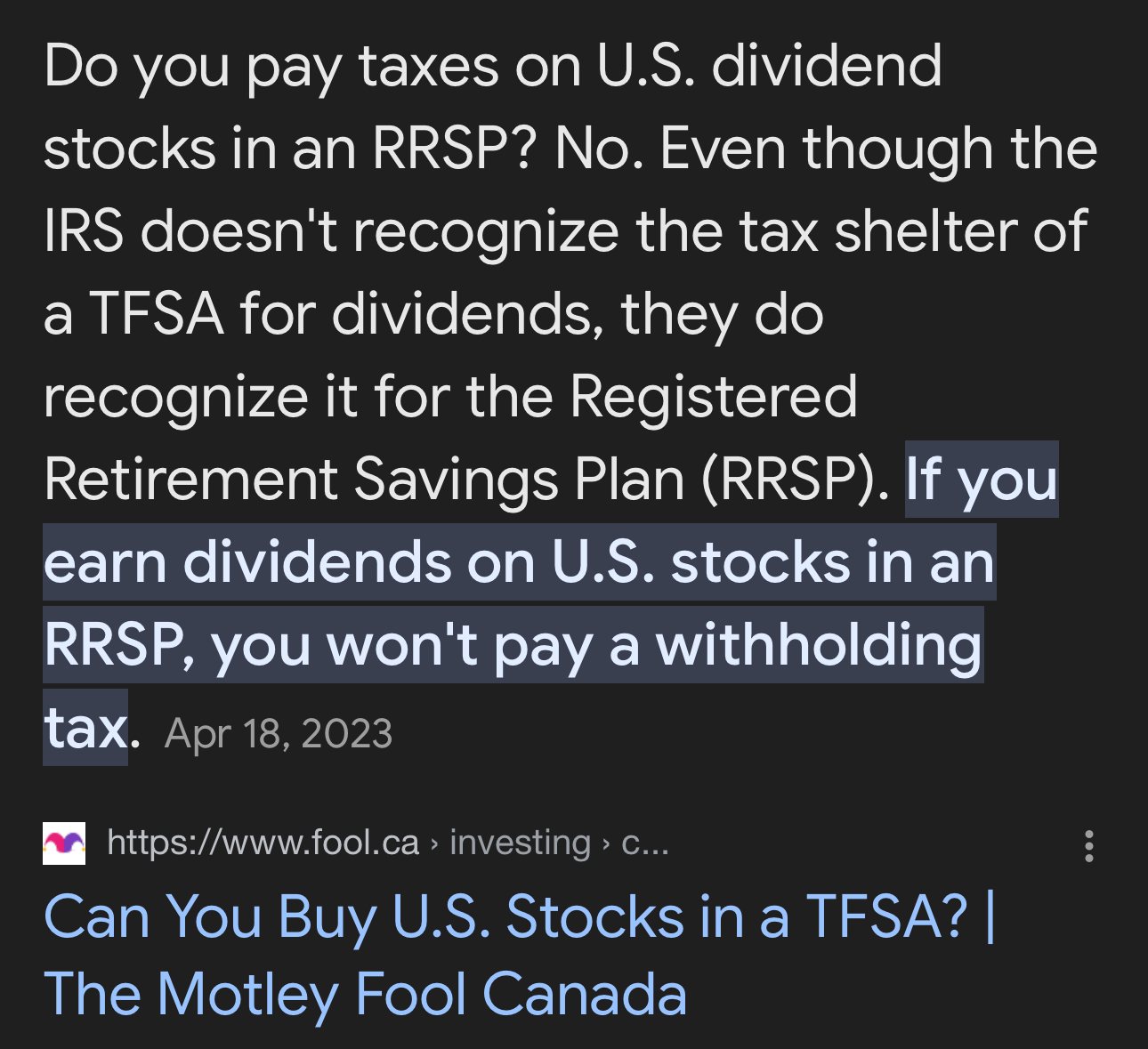

RRSP美股派Dividend唔係free tax咩?有無人有其他資料大家互對一下

如果想將來喺度買樓應該努力工做儲錢

唔係買或者唔買RRSP

唔係買或者唔買RRSP

上年用app報稅 今年上cra my account填哂SIN都拎唔到個number 退稅封信都無number 點搞

退稅封信都無number 點搞who own the house?

plus interest income from the day you entered Canada convert everything to Canadian dollar on the day you entered.

https://www.moneysense.ca/columns/ask-a-planner/us-withholding-tax-in-an-rrsp-for-canadians/#:~:text=U.S.%20stock%20dividends%20paid%20into,deferred%20status%20of%20the%20accounts.

Qualifying to reclaim U.S. withholding tax

In order to qualify for the lower rate, an investor has to fill out the Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals) and provide it to their investment firm. These forms are generally valid until the end of the third calendar year after signing, so need to be re-signed every three years.

U.S. stock dividends paid into an RRSP, registered retirement income fund (RRIF) or a similar registered retirement account are generally free from withholding tax for Canadian residents, as the U.S. recognizes the tax-deferred status of the accounts. In non-registered and tax-free savings accounts (TFSAs), the reduced 15% rate generally applies.

If excess tax is withheld, it can be recovered by filing a U.S. tax return. However, the time and cost may be more than the potential refund unless the withholding tax is significant.

An important point is that Canadian mutual funds and exchange-traded funds (ETFs) that own U.S. stocks are considered Canadian residents and are subject to 15% withholding tax. If you own these in your RRSP, they will not qualify for the 0% withholding tax rate. This is because the mutual fund or ETF is considered the shareholder of the U.S. stocks, not you or your RRSP. (Try MoneySense’s ETF screener tool.)

The best RRSP rates in Canada Compare now

EDP dividends for Canadians

In your case, Wanda, you own shares of Enterprise Products Partners, which is a master limited partnership trading on the New York Stock Exchange (NYSE). Based on the current quarterly dividend and stock price, the annual dividend yield is about 7.6%.

A master limited partnership (MLP) is a U.S. publicly traded entity that is taxed as a partnership, rather than a corporation. Most stocks on U.S. exchanges are corporations paying dividends.

MLPs do not generally pay income tax, instead distributing their income to the unitholders or “partners,” as opposed to a corporation that pays its after-tax profits to shareholders. However, U.S. MLPs can elect to be taxed as a corporation.

A Canadian resident unitholder of an MLP, like EPD, is generally considered to be a partner carrying on a trade or business in the U.S. The tax withholding rate is equal to the top U.S. marginal tax rate of 37%, Wanda, unless the partnership elects to be taxed as a corporation in the U.S.

A Canadian investor who owns an MLP is technically required to file a U.S. tax return to report this U.S.-source income. The U.S. tax reporting (schedule K-1) may not be easy to use to convert the U.S. income for Canadian tax purposes for non-registered accounts. This is a drawback of owning U.S. MLPs.

In addition, if the dividends are subject to 37% withholding tax in a tax-sheltered account like an RRSP. They are also subject to additional Canadian tax payable on a withdrawal in the future, there may be an element of double taxation for Canadians owning MLPs, Wanda.

So, the moral of the story here is that the high yield of EPD is a bit of a trojan horse for a Canadian investor. There is a high withholding tax rate that applies, potential double taxation, and even tax filing complexities as well. Canadians should think twice about buying U.S. master limited partnerships.

Qualifying to reclaim U.S. withholding tax

In order to qualify for the lower rate, an investor has to fill out the Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals) and provide it to their investment firm. These forms are generally valid until the end of the third calendar year after signing, so need to be re-signed every three years.

U.S. stock dividends paid into an RRSP, registered retirement income fund (RRIF) or a similar registered retirement account are generally free from withholding tax for Canadian residents, as the U.S. recognizes the tax-deferred status of the accounts. In non-registered and tax-free savings accounts (TFSAs), the reduced 15% rate generally applies.

If excess tax is withheld, it can be recovered by filing a U.S. tax return. However, the time and cost may be more than the potential refund unless the withholding tax is significant.

An important point is that Canadian mutual funds and exchange-traded funds (ETFs) that own U.S. stocks are considered Canadian residents and are subject to 15% withholding tax. If you own these in your RRSP, they will not qualify for the 0% withholding tax rate. This is because the mutual fund or ETF is considered the shareholder of the U.S. stocks, not you or your RRSP. (Try MoneySense’s ETF screener tool.)

The best RRSP rates in Canada Compare now

EDP dividends for Canadians

In your case, Wanda, you own shares of Enterprise Products Partners, which is a master limited partnership trading on the New York Stock Exchange (NYSE). Based on the current quarterly dividend and stock price, the annual dividend yield is about 7.6%.

A master limited partnership (MLP) is a U.S. publicly traded entity that is taxed as a partnership, rather than a corporation. Most stocks on U.S. exchanges are corporations paying dividends.

MLPs do not generally pay income tax, instead distributing their income to the unitholders or “partners,” as opposed to a corporation that pays its after-tax profits to shareholders. However, U.S. MLPs can elect to be taxed as a corporation.

A Canadian resident unitholder of an MLP, like EPD, is generally considered to be a partner carrying on a trade or business in the U.S. The tax withholding rate is equal to the top U.S. marginal tax rate of 37%, Wanda, unless the partnership elects to be taxed as a corporation in the U.S.

A Canadian investor who owns an MLP is technically required to file a U.S. tax return to report this U.S.-source income. The U.S. tax reporting (schedule K-1) may not be easy to use to convert the U.S. income for Canadian tax purposes for non-registered accounts. This is a drawback of owning U.S. MLPs.

In addition, if the dividends are subject to 37% withholding tax in a tax-sheltered account like an RRSP. They are also subject to additional Canadian tax payable on a withdrawal in the future, there may be an element of double taxation for Canadians owning MLPs, Wanda.

So, the moral of the story here is that the high yield of EPD is a bit of a trojan horse for a Canadian investor. There is a high withholding tax rate that applies, potential double taxation, and even tax filing complexities as well. Canadians should think twice about buying U.S. master limited partnerships.