https://www.bogleheads.org/forum/viewtopic.php?f=10&t=272640&p=4426315#p4424417

更舊既data會受佢地參考既拆息率對象所影響 (LIBOR vs fed rate etc)

另一個問題係weekend會白食個rate

---

I think I finally got to the bottom of this. LETFs just do NOT resell their swaps (or futures) entire positions at the end of the day ...This may involve some buying/selling of their regular index positions as well as some buying/selling of their swap/future positions, but this is an INCREMENTAL process.

...

The indirect implication of such incremental considerations is that, at the end of the week (or before a holiday), the LETF keeps its position with swaps/futures, according to the targeted market exposure. And then

over the week-end/holidays, well, the borrowing costs keep adding up.

...

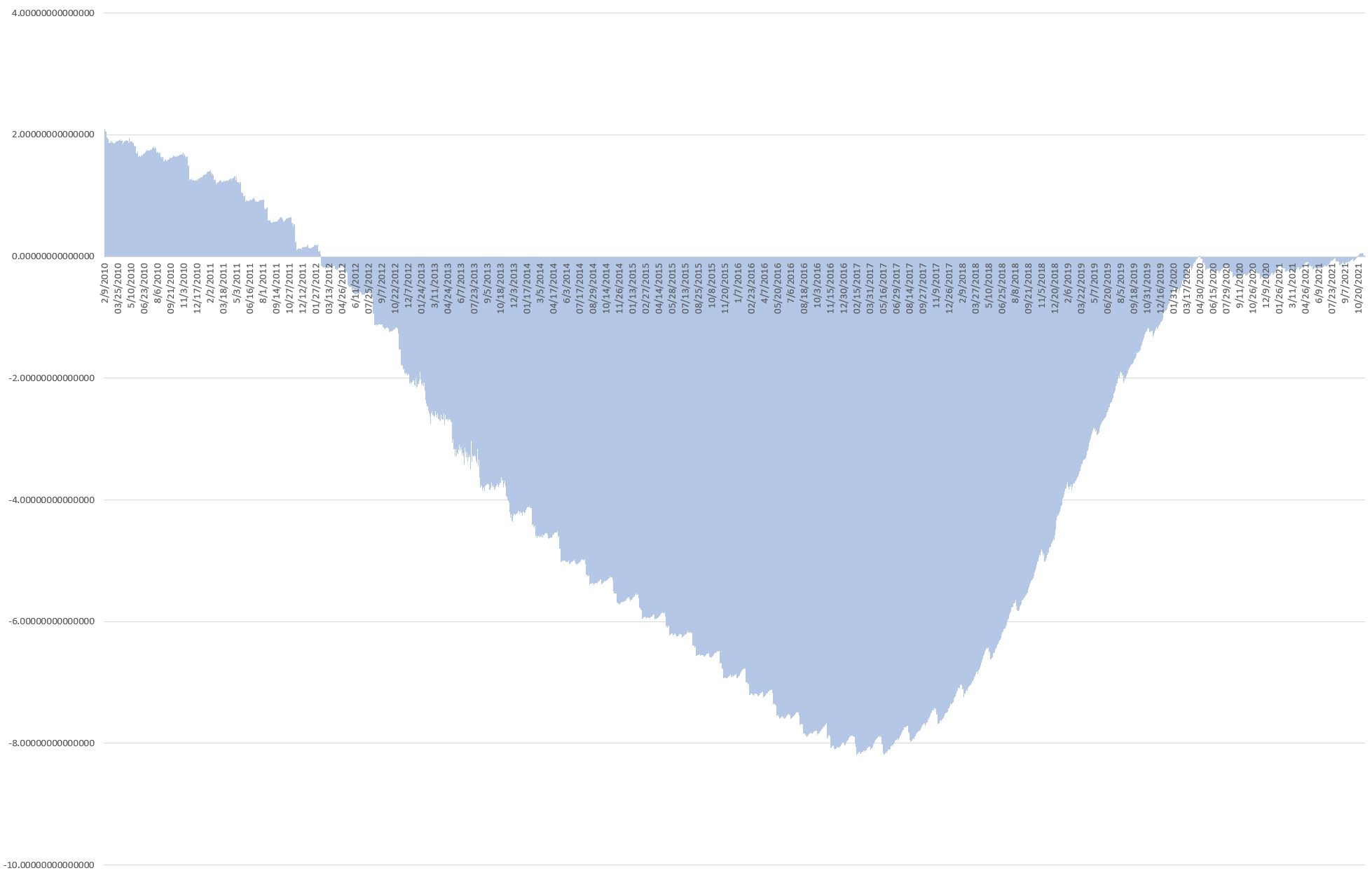

I actually verified it by comparing the MSCI USA Leveraged 2X data series to the theoretical 2x leveraged model...when using a LIBOR/overnight data series while forcing the non-trading days to zero borrowing costs, this just doesn't match.

When using a LIBOR/overnight data series while leaving the rates as is for non-trading days, funny, it matches perfectly. Same applies to S&P 500 Leveraged/Inverse 2x data series (I'll discuss special considerations about the regular S&P 500 leveraged series in the next post). And as I'll explain later, this also better matches the LETF actuals. A solid reasoning confirmed by empirical data from multiple independent sources, I think we're on solid ground here.