p 牌唔可以推post 只可以重開 請見諒 原po :

嘗試用數據分析下香港樓市

- 分享自 LIHKG 討論區

https://lih.kg/3978999

見到有巴打問source同code, 我將係post到有用到既data source 打出黎 :

第一個post :

CCL:

https://hk.centanet.com/CCI/query/data?type=CCL

CCL rent return %:

https://hk.centanet.com/CCI/query/data?type=CRI

hibor:

https://www.hkma.gov.hk/media/eng/doc/market-data-and-statistics/monthly-statistical-bulletin/T060302.xls

今次post 既data source:

以下既stationary test 我都係用測估處既data 因為有長D 時間同唔同大少單位既data

https://www.rvd.gov.hk/tc/publications/property_market_statistics.html

CNY:

https://www.investing.com/currencies/cny-hkd-historical-data

大陸房價:

https://m.gotohui.com/fangjia

code :

遲d 再update 依家寫到好亂

#2 factors 之間既互動

我test 過唔同既factors (包括測估處中唔同既單位既樓價指數,租金指數,HSI,CNY,hibor, GDP, median income, 失業率,CPI , 商鋪指數, S&P etc) 同樓價既spread 或ratio 有無siginicant stationary process ,發現以下三個係siginiciant (p-value <0.05) :

1. 測估處樓價指數 - CNY

Results of Dickey-Fuller Test:

Test Statistic -3.014902

p-value 0.033526

#Lags Used 0.000000

Number of Observations Used 399.000000

Critical Value (1%) -3.446846

Critical Value (5%) -2.868811

Critical Value (10%) -2.570643

Data is stationary

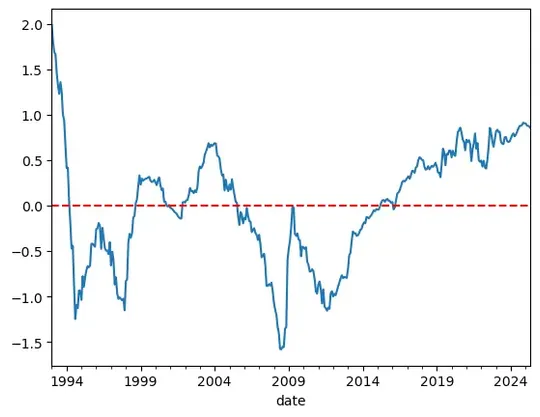

2. 測估處(40 平方以下) 租金指數 (表示為rent_A) - 測估處(160 平方或以上) 租金指數 (表示為rent_E)

Results of Dickey-Fuller Test:

Test Statistic -3.032980

p-value 0.031927

#Lags Used 6.000000

Number of Observations Used 382.000000

Critical Value (1%) -3.447585

Critical Value (5%) -2.869136

Critical Value (10%) -2.570816

Data is stationary

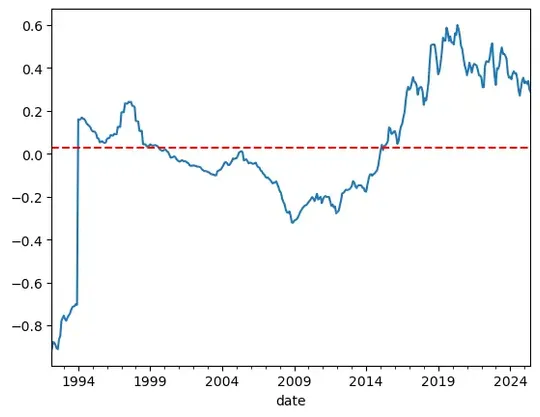

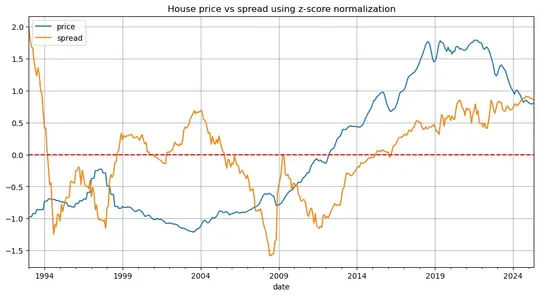

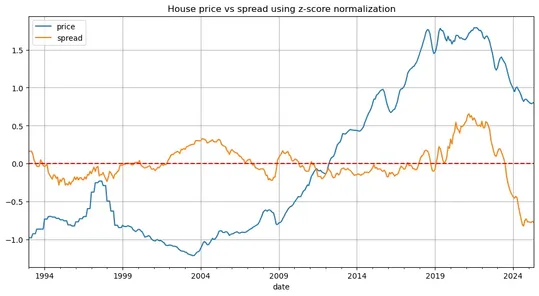

3.測估處(40 平方以下) 樓價指數 (表示為price_A) - 測估處(40 平方以下) 租金指數 (表示為rent_A)

Results of Dickey-Fuller Test:

Test Statistic -3.410066

p-value 0.010620

#Lags Used 13.000000

Number of Observations Used 375.000000

Critical Value (1%) -3.447909

Critical Value (5%) -2.869278

Critical Value (10%) -2.570892

Data is stationary

Summary :

首先price A 同測估處整體既房價指數correlation =1 , 即price A 可以視為整體房價既一個proxy

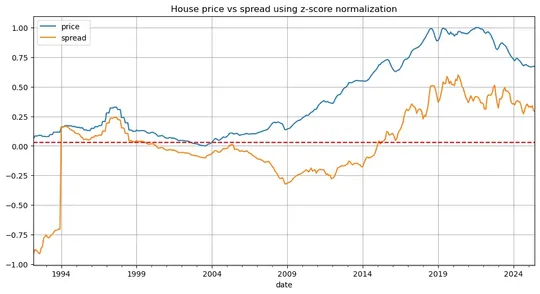

如果assume stationary process still hold, 極端既spread 會被修正,上面既factors 應該要如expectation column 中行走,但我認為pair 3 (price A -rent A) 既修正方式會以同方向(e.g price A , rent A 一齊升或跌)去修正,多過反方向修正(即price A 升,rent A 跌),原因如下:

樓價自2020年左右跟租金指數背馳,但其實兩者correlation 一直都是0.97 ,要expect 依兩個factors 繼續用背馳既方式(即priceA 升,rentA 跌) 去修正spread , 即期望租既人因為「供平過租」轉租為買,但因為現時hibor 升回2%以上,如果整個月還是2%以上 ,原post 的net 租金回報率已經跌穿其長期平均線,供平過租帶動背馳的方式修正spread 的可能性減少

咁如果我expect 租金跟樓價返回同步 究竟同升還是同跌才有效修正spread?

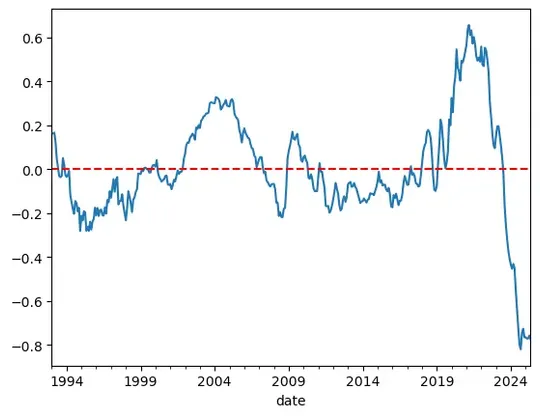

Z-score normalization 後,現在price A - rent A 的spread 為-0.775957 ,如果expect price A 同rent A 變番同升同跌,咁一齊跌係比一齊升更有效修正spread ( 變回less negative 如上圖)

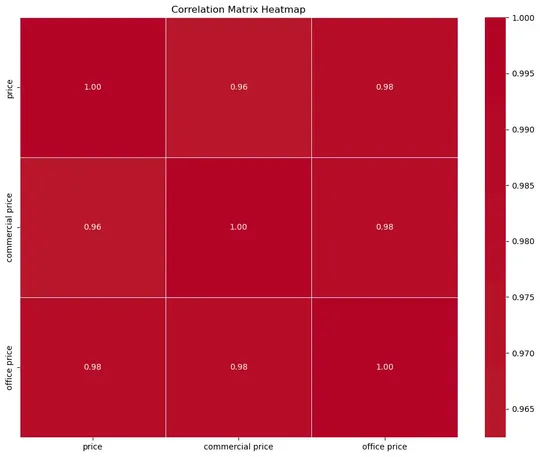

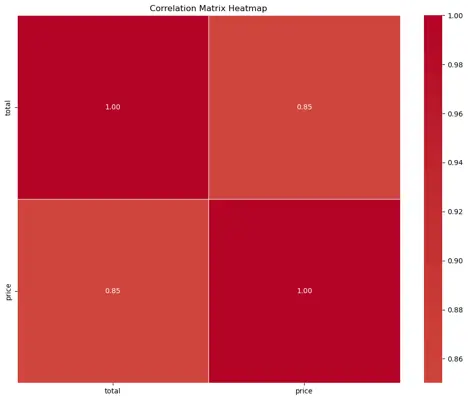

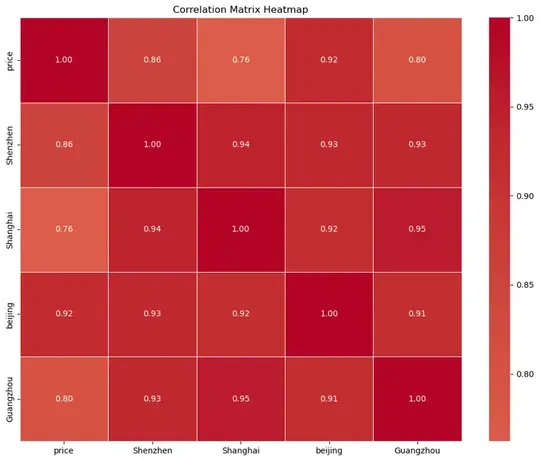

題外話,雖然有人話香港樓價見底,但我無咩聽過有人話香港工廈鋪見底,都無咩聽到有人話大陸樓價見底,但其實佢地同香港樓價correlation 唔低

香港(price) vs 百城房價 (total) correlation

香港(price) vs 大陸一線城市 correlation

住宅(price) vs 工商夏 correlation