Soxl 美帝ai晶片教 起壇!!!

wsb_refugee

195 回覆

28 Like

17 Dislike

特價時段一瞬即逝唔明驚what

總之我永遠見到佢個位數我就會買,講緊一件都$9我就開倉位

之後佢每跌一蚊我就溝,去到見到開始回升,市場開始興奮直頭開埋孖展大手買入

至少我係咁樣對待soxl 去到牛市嗰陣時你會見到呢隻股票搞到你個倉個總值每日都幾萬幾萬咁跳,好爽㗎

去到牛市嗰陣時你會見到呢隻股票搞到你個倉個總值每日都幾萬幾萬咁跳,好爽㗎

之後佢每跌一蚊我就溝,去到見到開始回升,市場開始興奮直頭開埋孖展大手買入

至少我係咁樣對待soxl

去到牛市嗰陣時你會見到呢隻股票搞到你個倉個總值每日都幾萬幾萬咁跳,好爽㗎勁

但唔怕佢跌得太低合股?

呢啲真係大心臟

風險唔高點會趺到個位數

甘冒風險抵你賺

風險唔高點會趺到個位數

甘冒風險抵你賺

會升返$50 財自機會到了

今日$9溝咗,均價大約$12

入定貨差唔多 業績期隻隻semi爆升跟本追唔返

均價12.5都要輸 幾時先追得返

幾時先追得返

幾時先追得返台仔電救唔救到

$TSM Reports Q1 (NT$) Net 361.6B v 346.8Be, Op 407.1B v 249.0B y/y, Rev 839.3B v 592.6B y/y (TSMC)

- Rev $25.5B +35.3% y/y, -5.1% q/q v $25.2Be

- Capex $10.1B v $7.1B q/q and $5.8B y/y

- Op margin: 48.5% v 42.0% y/y and 49.0% q/q

- Gross margin: 58.8% v 53.0% y/y

- Comments: In the first quarter, revenue decreased 3.4% quarter over-quarter, as our business was impacted by smartphone seasonality, partially offset by continued growth in AI-related demand. By technology, 3nm process technology contributed 22% of total wafer revenue in 1Q25 while 5nm and 7nm accounted for 36% and 15% respectively. Advanced technologies (7nm and below) accounted for 73% of total wafer revenue.

By platform, HPC and Smartphone represented 59% and 28% of net revenue respectively, while IoT, Automotive, DCE, and Others each represented 5%, 5%, 1%, and 2%. Sequentially, revenue from HPC, Automotive, DCE, and Others increased 7%, 14%, 8%, and 20% respectively, while Smartphone and IoT decreased 22% and 9% respectively.

From a geographic perspective, revenue from customers based in North America accounted for 77% of total net revenue in 1Q25 while revenue from China, Asia Pacific, Japan, and EMEA (Europe, Middle East, and Africa) accounted for 7%, 9%, 4%, and 3% of total net revenue respectively.

$TSM Reports Q1 (NT$) Net 361.6B v 346.8Be, Op 407.1B v 249.0B y/y, Rev 839.3B v 592.6B y/y (TSMC)

- Rev $25.5B +35.3% y/y, -5.1% q/q v $25.2Be

- Capex $10.1B v $7.1B q/q and $5.8B y/y

- Op margin: 48.5% v 42.0% y/y and 49.0% q/q

- Gross margin: 58.8% v 53.0% y/y

- Comments: In the first quarter, revenue decreased 3.4% quarter over-quarter, as our business was impacted by smartphone seasonality, partially offset by continued growth in AI-related demand. By technology, 3nm process technology contributed 22% of total wafer revenue in 1Q25 while 5nm and 7nm accounted for 36% and 15% respectively. Advanced technologies (7nm and below) accounted for 73% of total wafer revenue.

By platform, HPC and Smartphone represented 59% and 28% of net revenue respectively, while IoT, Automotive, DCE, and Others each represented 5%, 5%, 1%, and 2%. Sequentially, revenue from HPC, Automotive, DCE, and Others increased 7%, 14%, 8%, and 20% respectively, while Smartphone and IoT decreased 22% and 9% respectively.

From a geographic perspective, revenue from customers based in North America accounted for 77% of total net revenue in 1Q25 while revenue from China, Asia Pacific, Japan, and EMEA (Europe, Middle East, and Africa) accounted for 7%, 9%, 4%, and 3% of total net revenue respectively.

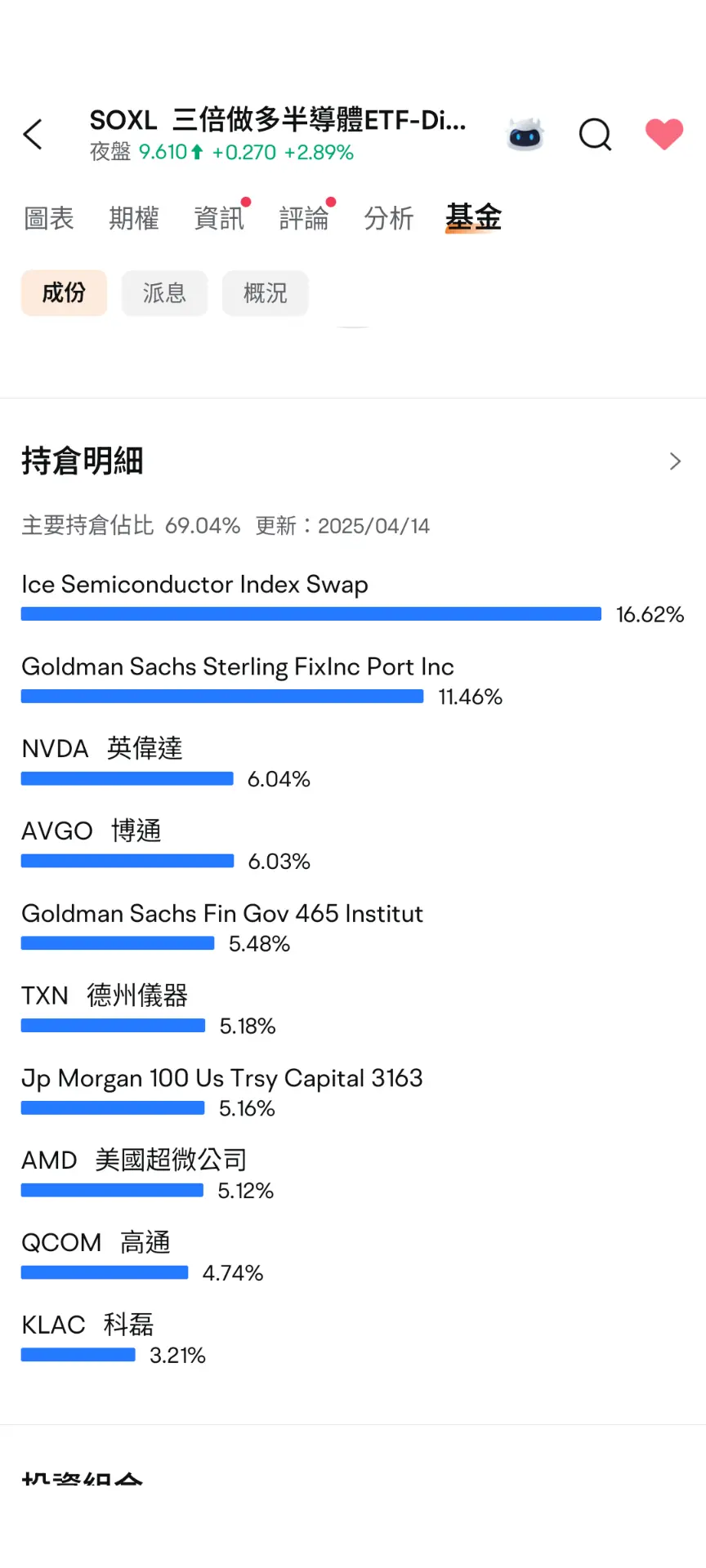

佢啲持倉好古怪

都唔知個fund 佬諗乜

上緊 陸續有來

好彩今日溝咗

仲以為intel 佔唔少添

依家重倉左Nvda每日都係幾萬幾萬咁跳

點解怪

點解咁廢日日都唔升係咪要等到芯片關稅出 樓主有信心佢出年升番?

係咪要等到芯片關稅出 樓主有信心佢出年升番?成個order board儲緊貨

點睇到?

佔得多一早合左股

之前有人話佢搞到23-24年Soxl 爆得唔夠上

學ict 睇圖

合股多數係反向etf , 正向又流通量高比較少

Set咗7.9入2000股