本文經刪減

Undoubtedly, Zoom Video Communications (ZM) has been one of the more popular stocks and companies amid the COVID-19 fears. However, while the stock has handily outperformed the market over the past month, I believe there is more downside risk to the name than upside potential

.

.Security vulnerabilities have increased recently which have increased concerns over the safety of using Zoom, which could ultimately cause customers to move away from the free trial over time. However, there currently seems to be no signs pointing to lower usage

. This could be a potential trend to look out for in coming weeks and quarters.

. This could be a potential trend to look out for in coming weeks and quarters.However, my bigger concern revolves around converting users from the free model to a paid version, increased security concerns, and valuation.

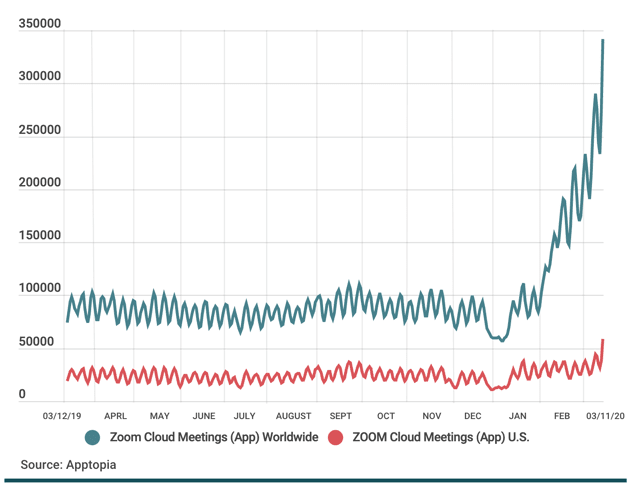

One report noted that Zoom's daily users increased to over 200 million in the month of March

, significantly greater than the previous high of 10 million (link to source page). The popularity of Zoom will likely continue to rise, but as long as the stock's valuation remains this high, I am cautious around this name.

, significantly greater than the previous high of 10 million (link to source page). The popularity of Zoom will likely continue to rise, but as long as the stock's valuation remains this high, I am cautious around this name.Q4 Earnings And Guidance Review

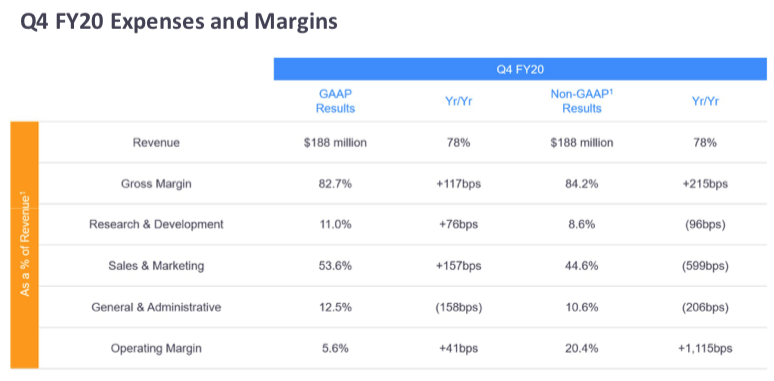

Combined with operating margin ~20%, this results in a near Rule of 100, significantly above the software industry norm of Rule of 40.

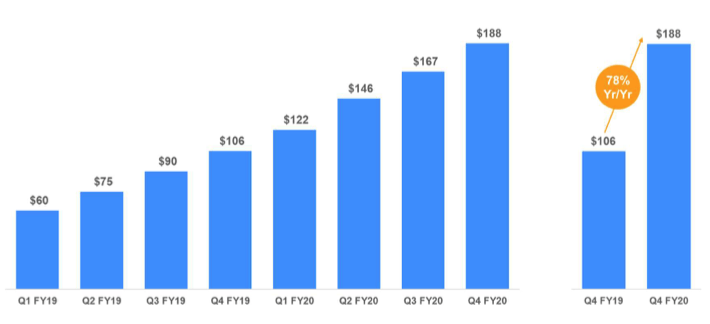

For the full year, management provided revenue guidance of $905-915 million, which represents 46% growth for the year, which compares to ~88% growth seen last year. However, I believe the early strength seen so far in Q1 will put the company well above expectations and we could see another year of revenue nearly doubling. In fact, I think there is a greater chance of revenue growth coming in at 100%+

than it coming in below.

than it coming in below.Security Concerns

However, it becomes a big concern when some market players start to not use Zoom due to privacy concerns and could shift to alternate solutions, such Microsoft Teams (MSFT), LogMeIn (LOGM), and Cisco (CSCO).

Even when looking at recent "News" from SeekingAlpha, headlines include:

"Senators told to avoid using Zoom"

"Zoom banned at Google"

"German foreign ministry restricts Zoom use"

"Zoom faces new suit, hires former Facebook CSO"

Larger companies who are looking to formalize a video conferencing host will likely increase their due diligence around Zoom and potentially look at other competitors.

But!

Reuters Social Media Sentiment Monitor, the social media sentiment is turning positive after a short period of being negative.

Valuation

Zoom has historically traded at a high premium when looking at revenue multiples given their unique combination of hyper-growth and solid profitability. However, valuation has ramped excessively in recent weeks as investors are starting to assume this hyper-growth to accelerate. I agree that revenue will likely remain solid for the next few quarters given the rapid transition of companies working-from-home, however, valuation should always be looked at when making an investment decision.

醬汁:

Zoom: Security Concerns And Valuation Make Investors Cautious

Zoom: Still Worth It

@SeekingAlpha